If you are familiar with Bitcoin, Ethereum, or cryptocurrency trading, you have certainly experienced the term "blockchain." But what is it, and why does everyone in the crypto universe talk about it?

Simply put, a blockchain is a decentralized, distributed ledger technology that can record transactions across several computers. You can think of it like a digital record book shared with thousands of people at the same time, where every record is permanent, and cannot be deleted or modified unnoticed.

Here are four attributes that distinguish blockchain: it is decentralized (it is not owned or operated by any level of authority), transparent (anyone is welcome to see the history of transactions), traceable (everyone transaction that happens will be indicated through a permanent trail), and immutable ( once the data has been placed on the ledger/made public, it cannot be changed).

To make this even simpler, let's think about it like this: Imagine a Google Sheet that is shared with millions of people across the globe. Anytime someone makes an edit, it immediately refreshes for everyone to view, and there is no way to delete or take away the record of those edits. This is basically how the blockchain operates, although greatly superior in security and sophistication.

In cryptocurrency, blockchain serves as the base that allows cryptocurrencies to function. For example, Bitcoin maintains a blockchain that records every transaction ever made on its network. Anyone is able to confirm these transactions and provides trust without the need for banks and/or governments as intermediaries.

The technology is made out of three critical components, or features: blocks of data stored in a chain (hence the name), cryptographic hashing to secure the data, and a network of verifiers (computers) to authenticate and maintain the records. This framework makes blockchain very secure and resilient to fraud.

The History of Blockchain: From Bitcoin to Modern Cryptocurrencies

The tale of blockchain began in 2008 when a person named Satoshi Nakamoto disclosed a revolutionary whitepaper that described Bitcoin. It gave rise to a new type of currency technology, which was essentially blockchain, that did not require the aid of banks or governments.

Bitcoin was truly the first instance of blockchain technology. It was meant only for peer-to-peer payments and a place to store value. The Bitcoin blockchain started in January 2009, and in the first actual Bitcoin transaction, a person bought two pizzas for 10,000 BTC (worth pennies at the time and millions today).

But blockchain did not stop there. In 2015, Ethereum launched and gave us the second generation of blockchain technology. Ethereum's significant innovation was in smart contracts, which are self-executing programs that run on the blockchain. Combined with its own currency (ether), the Ethereum blockchain opened the door to exponentially more use cases beyond simple payments. Developers could create decentralized applications (Dapps) for anything from lending applications to digital marketplace art.

To think about it, Bitcoin was a secure digital notebook for tracking money, and with Ethereum it was like upgrading to a full computer to run programs to automatically do anything you want.

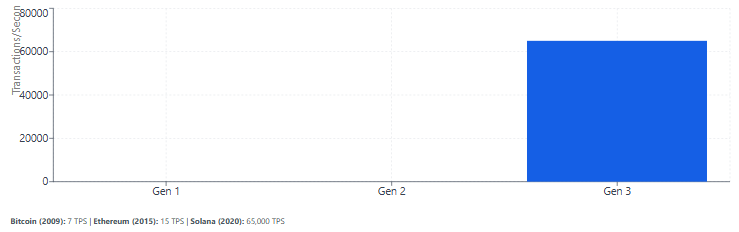

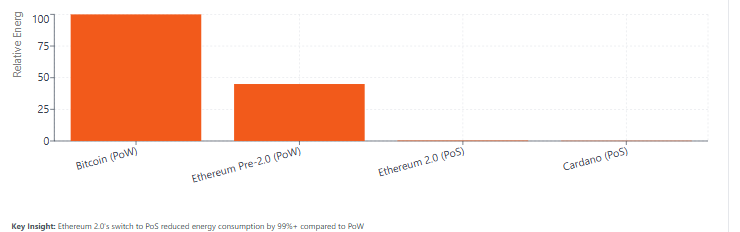

Today, there are third-generation blockchains coming to market. Projects such as Cardano, Solana, and Polkadot are addressing previous limitations, such as slower transaction speeds, greater energy use, and a lack of interoperability widespread across blockchains. These new third-generation platforms are effective in increasing energy efficiency through new consensus mechanisms, such as Proof of Stake rather than Proof of Work, and in enabling cross-chain communication.

Ethereum itself has evolved over recent months, beginning with its transition to Ethereum 2.0 which represents a major upgrade and a shift away from the energy-intensive Proof of Work model to a Proof of Stake, thereby significantly reducing the ecological footprint while improving scalability.

This evolution is ongoing. What began as an experiment in digital cash has turned into a significant ecosystem for decentralized finance (DeFi), non-fungible tokens (NFTs), decentralized autonomous organizations (DAOs) and many more applications that are causing us to rethink the meaning of digital ownership and transactions.

Core Technologies of Blockchain

When you understand how blockchain actually works, it helps you understand why it is so revolutionary. Let's examine the key technologies behind the workings of blockchain.

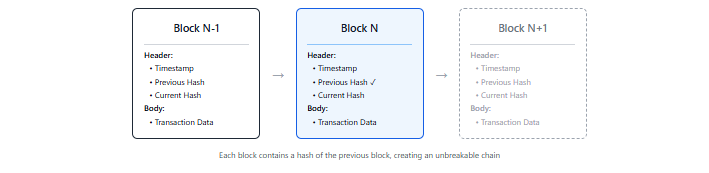

Block Structure: Each blockchain consists of individual blocks containing data. Each of these blocks has two main components: a header and a body. The header contains metadata, such as the timestamp, a reference to the previous block, and a hash (think of this as a digital fingerprint that is unique). The body of the block contains the data of the transaction.

The Concept of the Chain: Each block is linked together by cryptographic hashes. Each new block contains a hash of the previous block, and it would be impossible to break this chain. If a person attempts to alter any of the old blocks, the hash would change, breaking the chain of blocks, and the entire network is alerted. This design, for many reasons, makes blockchain incredibly secure and practically impossible to alter in the past.

Think of it as a classroom in which all of the students have a copy of the grade sheet which is the same grade sheet. If one student tries to alter their grade on their own grade sheet, by putting a different name or changing the mark, it is evident that all of the other students have the same grade sheet and that there is a discrepancy between the altered grade sheet and the original grade sheet.

Consensus Mechanisms

Given the decentralized nature of blockchain systems, it is important to establish a way for all actors to agree on what is considered valid. Consensus mechanisms accomplish this task. The most common types are:

-

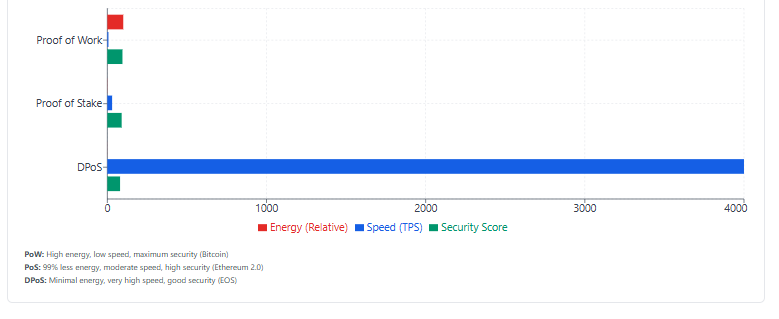

Proof of Work (PoW): Miners compete against other miners to solve a difficult mathematical problem. The first miner who solves the problem is rewarded with adding the subsequent block to the blockchain. Bitcoin uses this form of consensus mechanism, which requires an enormous amount of computational power and energy to secure the network.

-

Proof of Stake (PoS): The protocol randomly selects validators to create new blocks based on how many coins they have to "stake" as collateral. This requires much less energy than the PoW method. Ethereum has now implemented this system.

-

Delegated Proof of Stake (DPoS): Token holders participate by delegating their vote to selected representatives called validators. These validators then validate transactions on behalf of token holders, making the process faster and significantly more efficient.

Smart Contracts

Smart contracts are self-executing programs created and stored on the blockchain. The smart contract automatically executes when the terms of the contract are satisfied. For example, in a lending protocol on Ethereum, the smart contract can automatically transfer collateral if a borrower is unable to pay back their loan. This process does not require lawyers, courts, or other intermediaries.

The Decentralized Network Blockchain utilizes a decentralized network of nodes (computers running a blockchain application). The various participants can play different roles:

-

The nodes store copies of the blockchain and validate transactions

-

Miners (in PoW systems) perform puzzle solving and receive a right to add blocks to the existing chain

-

Validators (in PoS systems) stake their coins to validate the transactions and add blocks to the chain

This decentralized structure protects from a singular point of failure; if some of the nodes go offline, the network continues to operate (to maintain data integrity) with thousands of nodes storing copies of the data.

Blockchain in Cryptocurrency Trading

Blockchain technology has completely changed how we conduct trades of digital assets. Here’s why it’s important in trading cryptocurrencies and how it differs from traditional financial systems.

Transparency and Traceability: Each cryptocurrency transaction is recorded on the blockchain, and it is permanently visible. You can track any Bitcoin from when it was mined to where it is currently held in a wallet. This transparency allows for accountability without compromising user privacy (in which wallets are pseudonymous and not immediately associated with real-life individuals).

Do you want to verify a transaction? You simply go to a blockchain explorer such as Etherscan or Blockchain.com, enter the transaction ID, and you will see all the information: sending address, receiving address, the amount, timestamp, and transaction fee.

Decentralized Exchanges vs. Centralized Exchanges: The Blockchain led to the development of centralized exchanges (DEXs) like Uniswap or SushiSwap on. With a DEX, you conduct trades directly from your wallet using smart contracts. There’s no company holding your money, and as such you remain 100% in control of your funds.

Then there are centralized exchanges (CEXs), such as Coinbase or Binance, in which you deposit in the exchange’s custody. Many times, CEXs offer better liquidity and user experience than DEXs, however, DEX’s will put the user in full control and not risk an exchange hacking or freezing assets.

You could think of it this way: a CEX is like putting money in a bank vault, while a DEX is like you and a friend exchanging game points directly with everyone watching to ensure the trade is fair.

Transaction Security Blockchain solved the issue of double spending that plagued previous attempts at digital currency. In traditional digital systems, it was theoretically possible to copy the amount and spend the same digital money multiple times. Blockchain blocks this from happening through its consensus mechanism and distributed ledger. After a transaction is confirmed and contained in a block, it becomes irreversible, unlikely to be altered, or duplicated by all parties involved.

The nature of blockchain being cryptographically secure also allows it to prevent being tampered with or left vulnerable to fraud. Someone trying to alter the data of a confirmed transaction would need to hold more than 51% of the computing power on that network. While an individual can theoretically hack their way into a non-major blockchain to make this happen, it would be nearly impossible to do it for major blockchain infrastructure such as Bitcoin or Ethereum.

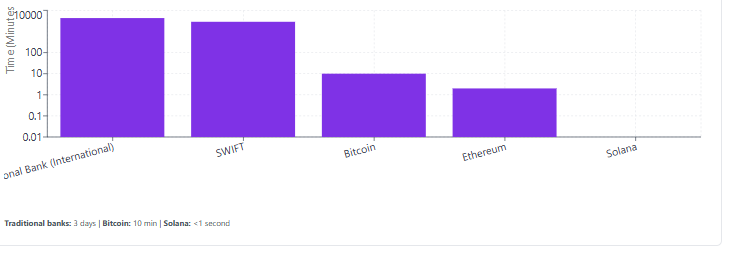

Settlement Speed Settlement refers to the speed at which the transaction is (completed). A traditional transfer of funds from one bank account can take several days to settle (and this is especially true for international transactions). However, transactions that take place on blockchain can settle within a few minutes and often within seconds, depending on the level of network congestion. A Bitcoin transaction, for example, typically settles in about 10 minutes. However, there are newer blockchains (e.g. Solana, which can process thousands of transactions per second).

Beyond Bitcoin: How Blockchain is Revolutionizing FinTech and Other Industries

Blockchain is making waves in areas far beyond cryptocurrency trading. The technology is indeed revitalizing whole industries and allowing for new feats that were not possible before.

FinTech Uses Banks and financial institutions, are utilizing blockchain in many ways with cross-border payments that increase speed from days to seconds and lower transaction costs through organizations like Ripple that provides banks with a method to transfer money quickly and safely. Traditional systems such as SWIFT take 3-5 days to settle and charge very high fees, whereas blockchain solutions settle almost instantly while costs to the end-user can be verified to be negligible.

Digital asset custody is another major use case for blockchain. Institutional investors now custodize billions of dollars of cryptocurrency and use blockchain custodial solutions which allow for assurance that the money is kept safe, secured, and regulatory according to the safety of a regulated financial institution.

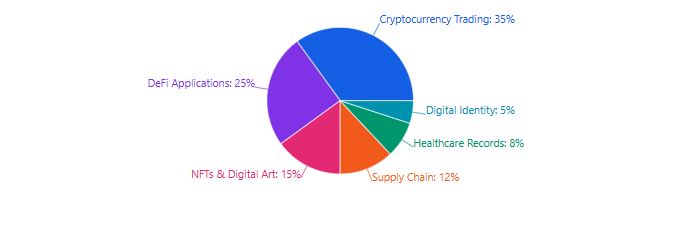

Product Supply Chain Tracking A number of companies including VeChain and IBM's Food Trust are using blockchain to track products from origin to consumer. For example, you buy a coffee and scan the QR on the package and immediately see the farm where the coffee came from, when it was harvested, how it was processed, and all the steps needed for it to get to your local café. This transparency is also a vetting tool to obtain some assurances that the product you are buying was not counterfeit, was sourced ethically and by vetting it builds trust with consumers.

Medical Records: Healthcare providers are investigating blockchain to develop secure, interoperable patient records. Rather than having your medical history spread across various hospitals and clinics, it could exist in a blockchain controlled by you. This promotes better care coordination while protecting privacy.

Digital Identity: Blockchain can provide self-sovereign identity solutions in which individuals own and control their own personal data rather than corporations. This could change everything from how you log into websites, to proving your credentials without disclosing sensitive information.

NFTs and Digital Ownership: Non-fungible tokens (NFTs) use blockchain to establish proof of ownership over digital assets. While digital art has been in the spotlight, NFTs are beneficial for gaming (owning in-game items), real estate (property title), intellectual property (music royalties), and ticketing (not allowing scalpers).

Blockchain Terms You Must Know: A Complete Crypto Glossary

Familiarizing yourself with blockchain terms will help you move through the crypto sphere with ease. Here are some of the key terms every trader should know:

Block: A collection of transaction data that is appended to the blockchain. It can be thought of as like a page in a ledger which can no longer be erased, once written.

Chain: A series of connected blocks that are linked through cryptographically secure hashes to the previous block. Each block points backward to the block that comes before it.

Node: A computer that connects to the blockchain network and holds a copy of the blockchain ledger and confirms transactions.

Hash: A unique digital fingerprint produced by a mathematical function. Hashing will take any input (a transaction, a block) and return a string of characters of fixed length - an input with even one tiny change will look completely different.

Consensus Mechanism: How blockchain agrees that transactions are valid. There are different mechanisms like Proof of work (PoW) and Proof of Stake (PoS) among others.

Smart Contract: Self-executing code that runs on the blockchain and executes actions automatically once a specific condition occurs. A good analogy would be to compare it to a vending machine: pay the specific amount and then get whatever you paid for without intervention.

On-Chain Transaction: Transactions that are logged directly onto the blockchain. They are permanent, transparent and can be verified by any third party.

Mining: The practice of utilizing computational power to solve complex puzzles, lose validated transactions and add new blocks to the blockchain. Miners receive payment in cryptocurrency for their contributions. You can visualize it as everyone in a room trying to solve a puzzle, and whoever solves it first, gets paid.

Gas Fee: A cost that is incurred to execute a transaction or smart contract on a blockchain such as Ethereum. The gas fee increases if there are a lot of transactions at the same time, as users are competing to have their transactions processed faster.

Double Spend: An attack in which someone attempts to spend the same cryptocurrency twice. The nature of the blockchain makes it incredibly difficult because the transactions are validated independently by the entire network with a distributed ledger.

Decentralized: A system operating free of a central authority. Instead of the network being controlled by one corporation or government entity, power is shared and distributed among all participants as needed.

Validator: Participants in Proof of Stake systems who put their cryptocurrency at stake to verify blockchain transactions and create new blocks. Validators earn rewards for acting honestly, but if they behave maliciously, they will lose their stake in the cryptocurrency.

Fork: An alteration to an existing protocol of the blockchain. A soft fork is a change that is backwards-compatible, whereas a hard fork creates a permanent separation from the original protocol and results in two separate blockchains. An example of a hard fork is when Bitcoin Cash was created and split from Bitcoin.

Advantages and Limitations of Blockchain

Like any other technology, blockchain comes with pros and cons. Knowing both pros and cons can help you make an educated decision about using and/or investing into blockchain based systems.

Pros:

Decentralization means that no one individual or organization controls the network. This eliminates single points of failure and decreases the risk of being censored or manipulated by an authority. A bank can freeze your account, but no one can freeze your cryptocurrency wallet.

Security is established through cryptographic security and distributed consensus. Unless a hacker compromises a majority of the network all at once, the expense and effort of hacking a blockchain is astronomically high - especially on a well-established chain.

Transparency allows anyone to verify transactions, and audit the system. It creates trust without needing a third party. If you didn't trust a bank, you could trust that your payment was executed on the blockchain and follow the transactions in data timestamps.

Immutability means that once it's recorded, it will always be in the system. Even without trust in the system, it creates an unchangeable historical record, which is ideal to use in tracking applications that need audit trails.

Cost-saving takes place because blockchain eliminates the intermediaries. For example, if you transfer money laterally across the globe, you don't pay correspondent banks to take every cut.

Limitations

There are still concerns associated with scalability. Bitcoin manages to fulfill about 7 transactions per second, while an organization like Visa performs on the order of thousands of transactions per second to keep up with demand. More users participating in blockchain networks means that those networks become bogged down or slow. This is also one of the reasons that there are third generation, and a layer two solution, blockchains being developed.

Energy consumption is indeed a topic of conversation; this primarily is a byproduct of Proof of Work blockchains. Bitcoin, as an entire cryptocurrency, consumes more energy than some countries! Energy consumption is a real concern and many valid factors to consider, although Proof of Stake systems, like Ethereum 2.0, is approx 99% less energy consuming than Proof of Work blockchains.

Transaction speeds fluctuate extremely. Some of the very recent blockchain examples just mentioned, are nearly instantaneous, whereas Bitcoin and Ethereum transactions sometimes increase to minutes or hours based upon traffic on the network. I think your class document was slow to refresh after you made contributions, and those improvements made it sluggish to respond.

Regulatory uncertainty raises some different questions from a risk perspective. Across the world, governments are attempting to scope out what proper regulatory framework they can enforce blockchain and cryptocurrency in their jurisdiction, and it is very much in flux.

Irreversibility is an issue, but it can also be a benefit! When you send cryptocurrency to an incorrect address, or are a victim of a scam, there is no customer service number to call for a refund; it is recorded forever.

Technical complexity sometimes is represented as a barrier. If you are okay managing your private keys, gas fees, and using the blockchain systems you have heard of you are way ahead of the learning curve that many potential participants find intimidating users.

The Future of Blockchain: Trends, DeFi, NFTs, and Digital Assets

Blockchain technology is advancing at a swift pace, and with each new milestone, it is transforming the ways in which we will be interacting with digital assets and decentralized systems in the future.

Technical Innovations

Over the last couple of years, we have learned about Layer 2 scaling solutions like Ethereum's Optimism and Arbitrum, which can effectively process transactions off the main blockchain before bringing a bunch of transactions back to the main chain in a single batch. The user experience dramatically increases speed and decreases costs, while still providing the benefits of security. You can think of this like a local shopkeeper taking their daily receipts to the bank, all at once, rather than dropping off each transaction by itself.

Cross-chain technology allows for different blockchains to communicate and exchange information. Projects like Polkadot and Cosmos are building "bridges" that allow e.g. you to seamlessly move an asset from one blockchain to another. This cross-chain communication capability has long been the Holy Grail of bridging the current and fractured blockchain ecosystem.

Energy-efficient consensus mechanisms are moving to replace energy-guzzling Proof of Work; its energy use has dropped by over 99% as a result of Ethereum's switch to Proof of Stake. We will soon see a brand-new blockchain launched with sustainable consensus, and launched that way from day one.

Application Trends

DeFi (Decentralized Finance) continues to grow into other aspects beyond lending and borrowing. Now we are seeing decentralized insurance, synthetic assets that track real-world prices, and algorithmic stablecoins. DeFi's total value locked exploded from almost nothing in 2019 - we are now observing the billions

NFTs are shifting from being for digital artistry to functional applications. Musicians are using NFTs to offer music directly to their fans and embed royalties payment. Real estate companies are testing property titles as NFTs. And game developers are creating play-to-earn environments, where in-game items are digital assets that can be exchanged outside of game with value.

Enterprise blockchain solutions are assisting large corporations in streamlining processes. Walmart uses blockchain technology to track food products, and shipping companies such as Maersk have applied blockchain to increase efficiency, and improve global trade by reducing paperwork.

Digital identity systems might allow you to have control over your person data. Instead of each App or website storing your data, you would have a blockchain-based identity that you control and can share only what is necessary for that interaction.

Investment and Adoption Trends

Meanwhile, throughout the overall transformation of the crypto landscape due to institutional investment, firms such as Tesla and MicroStrategy are holding billions of dollars in Bitcoin on their balance sheets. The large banks now offer cryptocurrency services to clients. Traditional investors have access to Bitcoin and Ethereum ETFs through traditional investment accounts without having to purchase the coin.

Dozens of nations are considering or testing Central Bank Digital Currencies (CBDCs). These digital currencies are government-backed and utilize blockchain technology while also allowing for a central authority. China's digital yuan is already widely being tested and many other countries are in the process of following.

More and more payment systems are being adopted. More retail stores are accepting cryptocurrency payments, and payment processors are beginning to integrate blockchain-based solutions. Banks are beginning to utilize blockchain technology to settle transactions in a transparent, faster, and more efficient manner—on the back end.

Begin Your Blockchain Journey Today

Blockchain is not just the technology behind cryptocurrency (Bitcoin), it is a big shift in the way we record, verify, and trust digital information. From a very narrow beginning as the underlying technology behind cryptocurrency, blockchain technology is now being used across verticals. Blockchain provides transparency, security, and decentralization that no existing payment system can replicate.

You now know that blocks are built up in a chain form, how consensus mechanisms ensure integrity of the network, and how smart contracts enable automated complex agreements without third parties. You understand the differences between PoW and PoS, why gas fees exist, and how blockchain allows decentralized exchanges and supply chain tracking.

However, understanding blockchain goes beyond simply learning the definition of terms. It is important to understand how it can revolutionize finance, reshape industries, and create new opportunities for those who wish to learn and become involved. Whether you are intrigued by trading cryptocurrency, developing decentralized applications, or just seeking an understanding of the technology that is reshaping our digital future, you now have the capacity to do so.

To be clear, blockchain and any technology, has limitations. Scalability, energy consumption, and regulatory uncertainty are real issues. But solutions are developing through Layer 2, proof-of-stake, and new frameworks that serve to solve scalability and usability issues, at the same time protecting many of the benefits of blockchain.

Stop reading about blockchain and start experiencing it for yourself. Create your BTCDana account now and trade your first cryptocurrency in a secure environment where you independently control your learning pace, because you learn blockchain by using and experiencing it for yourself.