Money is the driving force of the world, and the financial institution is the engine that moves the world. Whether you are setting up your first savings account, trading foreign currency, or wanting to know how the global market actually works, understanding financial institutions is your path to making knowledgeable financial decisions.

What Is a Financial Institution? – Definition and Primary Functions

Consider financial institutions as the pulse of the global economy. Financial institutions are intermediaries between people with money and people needing money. Financial institutions are not just for storing money or making payments; they are the link that allows institutions to be employed throughout the economy.

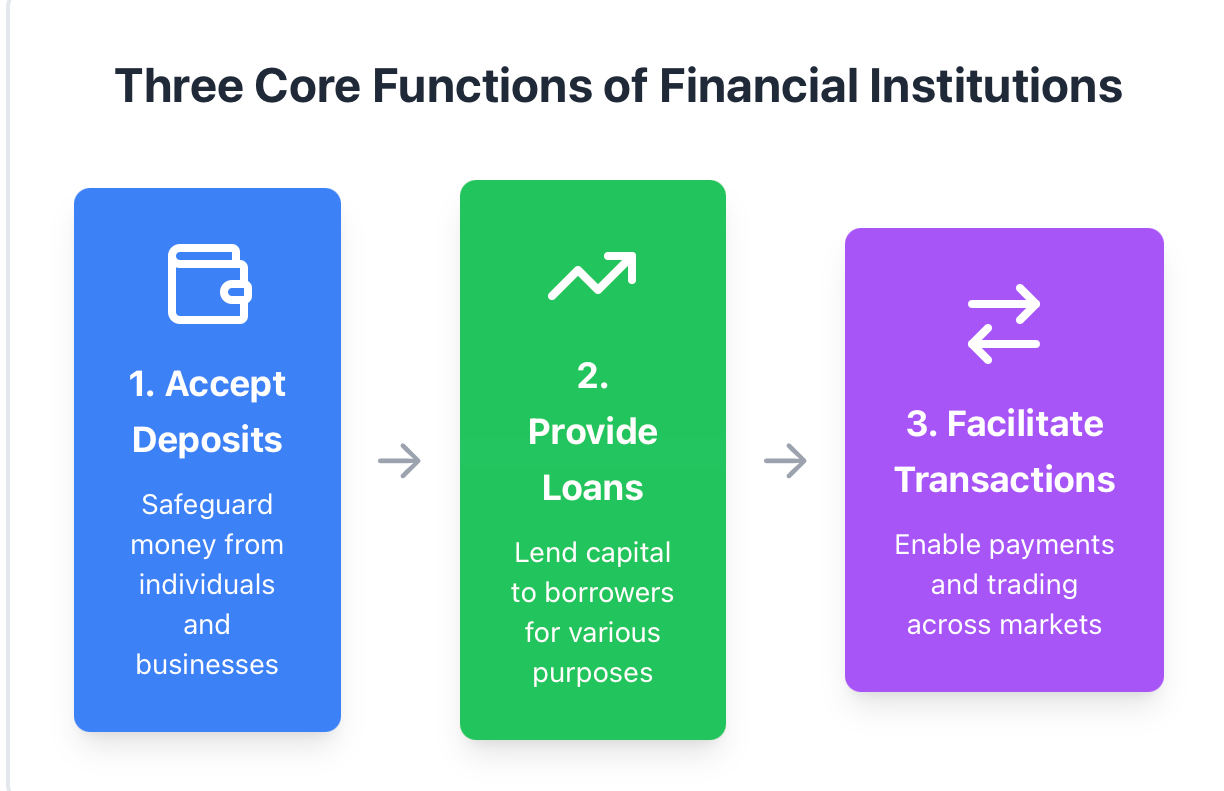

Financial institutions perform some basic, crucial functions. First, they accept deposits from people and companies who want to keep their money safe. Second, they lend money to people who need money to purchase homes, buy cars, and start businesses. Third, they invest in various assets, trade securities, and make payments from one source to another.

Professional Example: For example, JPMorgan Chase manages trillions of dollars of assets for various establishments and enables mortgage loans in a timely fashion as well as currency exchanges in various countries. When a worldwide company needs to move money across country lines or hedge their currency risk, JPMorgan or other institutions can provide the infrastructure, resources, and services to do that.

More Simplicated Example: Think of a bank as a library for money. Banks collect "books" (deposits) from "readers" (savers) who want to put their money away for safekeeping and lend that money to "readers" (borrowers).You receive a small amount of interest on your savings (rewards points can be considered an example), while the person borrowing money will be paying interest (like a late fee, but in a more predictable way). The bank works hard to service this transaction and affirms everyone leaves satisfied.

These providers of service are on a vast spectrum, including traditional banks that you use to cash checks and have checking accounts, investment banks that assist companies in raising capital, insurance companies that ensure you are compensated for the loss of a prized possession, and the platforms you utilize to buy and sell stocks or trade Forex currency pair options on the days you feel most confident about the transactions you are about to make. All are necessary services, and while they play different roles, it’s these roles, collectively, that form a critical scaffolding for the framework of modern financial markets.

Understanding their role is not simply something to pick up in the economic or finance courses you will take; whether intended or not, understanding these institutions, anticipating their motives, or even learning how to engage with them, will affect your capacity to invest, trade, or make the important financial decisions you will need every day.

Major Types of Financial Institutions You Should Know About

The financial markets have built a complex ecosystem with the services and functions different institutions provide. Let’s take a closer look at the major institutions.

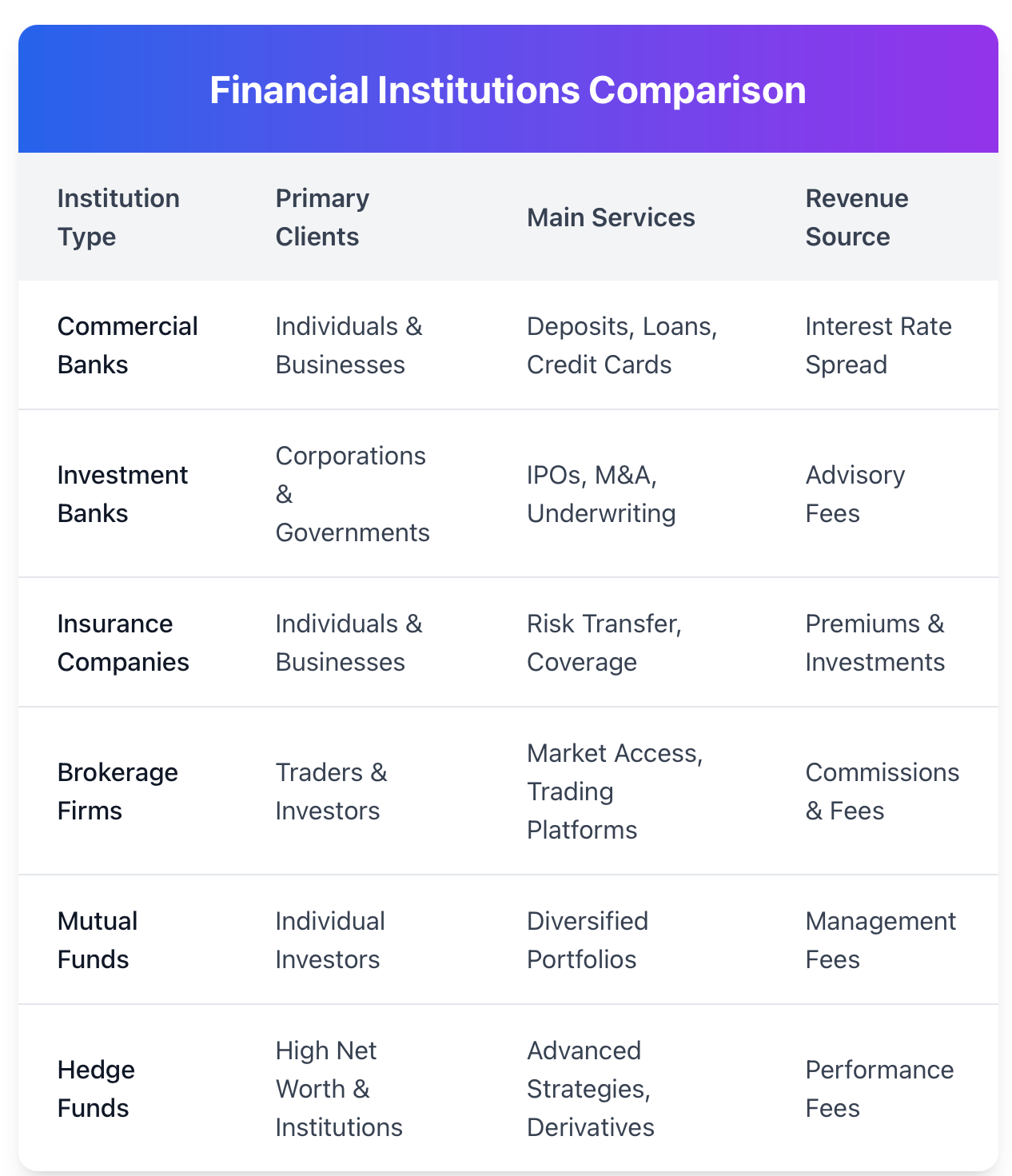

Commercial Banks are likely the most familiar institutions. They are the retail channel, where you handle check writing, savings deposits, personal loans, or credit cards for your expenses. Commercial banks also consult on financial aspects for companies and stores in the form of working capital loans, merchant services, and investment portfolio management. Commercial banks primarily earn from interest rate spread, they loan the money you deposit and pay (less) interest for deposits.

Investment Banks operate on an entirely different plane, ideally representing corporations and governments rather than the everyday individual consumer. For example, if a company takes the IPO route to a new source of capital, it was the investment bank which underwrite the offering and received any sort of takeover data of where to go to locate potential, permittedFirms provide advisory services in mergers and acquisitions, work to help companies raise capital through bond offerings, and serve a market-making function to provide liquidity to the financial markets.

Professional Example: Goldman Sachs advised on the merger between two technology powerhouses, structuring the merger and helping to navigate regulatory issues. Their prowess in valuation and understanding of the market conditions proved to be an asset in assisting the parties to complete the multi-billion-dollar deal.

Beginner-Friendly Example: You keep your savings at a standard bank where you earn maybe 1% interest a year. That is your compensation for allowing the bank to use your money. The bank will take that money and lend it out to borrowers at 5% to 7% for personal loans. The bank pockets the difference in interest and understands some will not repay their loans, so they have to manage risk.

Insurance Companies are specialists in risk management. They will pool premiums from policyholders and use actuarial science to forecast a claim, and then invest those premiums for a return. From life insurance to property coverage to protecting derivatives, they provide individuals and corporations the ability to transfer risk.

Brokerage Firms facilitate transactions responsive to traders and investors. They provide access to a stock market, a foreign exchange platform, future exchanges, and now, cryptocurrency trading. Contemporary brokerages like Charles Schwab or Interactive Brokers provide real-time data, educational tools, and platforms to receive investment capital as traditional needs.

Mutual Funds and Credit Unions fill unique niches. Mutual Funds will solicit many people for a pool of money to create a properly diversified portfolio of stocks, bonds, or other investments for smaller investors to allow for practice.Credit unions are nonprofit institutions organized by their members, and typically offer better rates than commercial banks because they do not try to extract as much profit for shareholders.

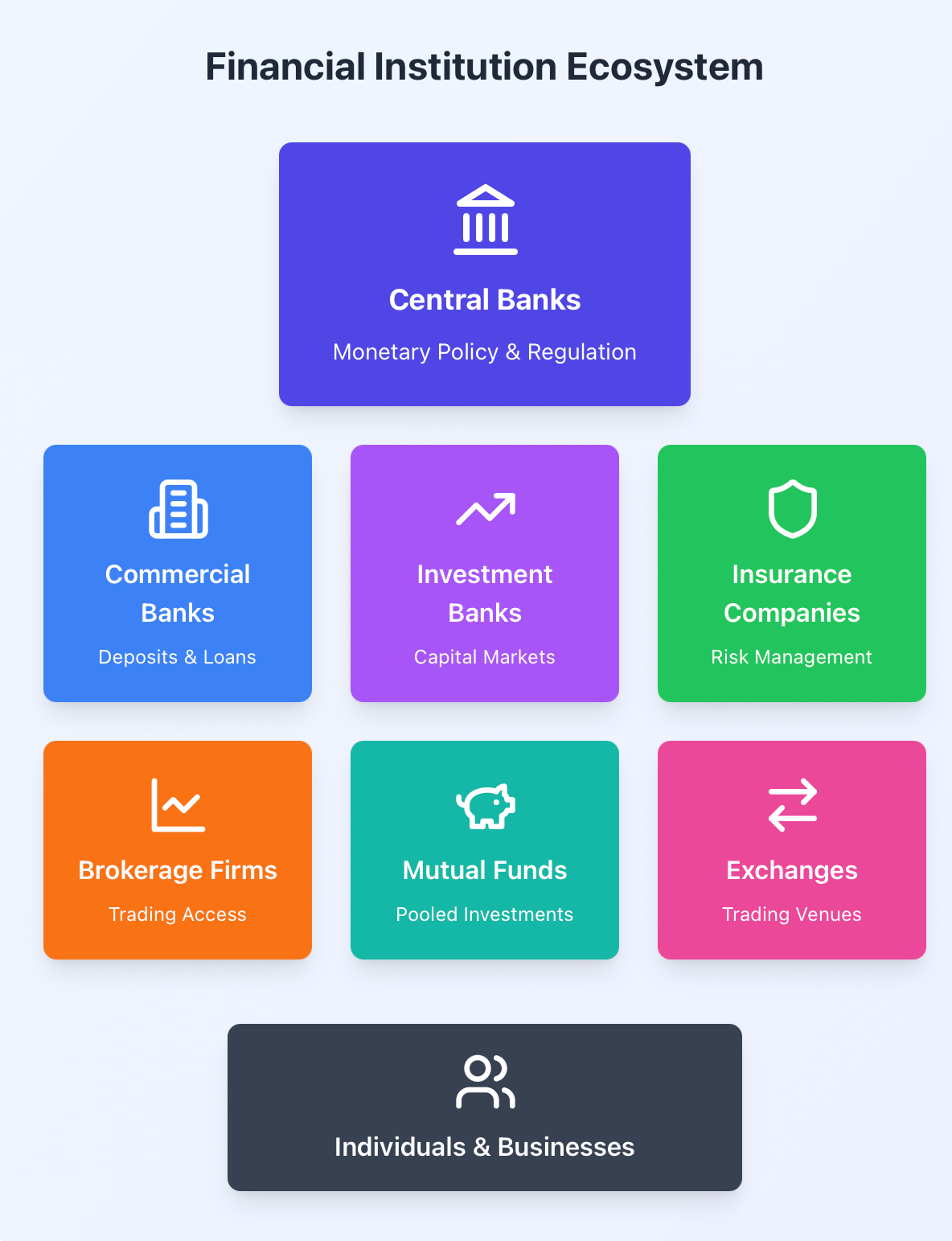

At the top of the financial ecosystem are central banks. The Federal Reserve, European Central Bank, and the Bank of England set monetary policy and interest rates, regulate the banking sector and act as a lender of last resort when all fails. When central banks make decisions, they almost always impact the rest of the financial ecosystem and the economy. The exchanges (such as NASDAQ, New York Stock Exchange, CME Group, or the Binance Exchange) are the marketplace where the actual transactions take place.

Exchanges are the marketplace that establishes the rules and allows buyers and sellers to match up. Exchanges also work with clearing houses that settle the trades. Hedge funds typically invest more aggressively than individual investors may be willing to. Hedge funds seek a return through lending, derivatives, short sales, and a variety of more advanced and sophisticated arbitrage strategies to make a return irrespective of the market direction. An example of a hedge fund that invests billions with institutional investors and high net worth clients is Bridgewater Associates.

Private equity firms will directly invest in private businesses or acquire publicly traded companies to delist them. Industry leaders such as Blackstone or KKR will restructure and cut costs before selling them for profit. Trust companies manage wealth, estates, and assets for clients. Trust companies frequently create client trusts for estate planning or while managing corporate pension funds.

Microfinance Institutions specialize in serving a population often neglected by traditional banking institutions. They provide small loans, savings vehicles, and financial education to business owners in developing economies and are a significant contributor to complimentary economic development.

Each institution serves its purpose within the financial system. There is some overlap in their services, but with a few exceptions, the institutions have defined functions and the work and details of the specific institutions help facilitate other and separate economic activities.

Impact of Financial Institutions

Financial institutions do not just participate in markets; they define them. The collective actions of financial institutions determine exactly where capital flows, which assets are increased or decreased, and how liquid assets are at the present time.

When large institutions make market movements, there is almost an immediate reaction in the market. Capital flows create liquidity by making it easier to buy or sell an asset without dramatically changing its price. For example, if JPMorgan or BlackRock allocate billions of dollars to U.S. Treasury bonds, the cost of those bonds will typically drop. Because bond prices and bond yields represent an inverse relationship, yields will fall, often creating downward movement in the yield of the broader market (lower aspects tend to follow lower yields). Mortgage rates are impacted and so is the dollar's strength by this one action.\

The impact of the investment decisions of the largest financial institutions can also create trends from which retail traders would potentially follow. If major hedge funds will begin shorting a particular sector, then other market participants will notice and shift their positions as well.

Professional example:

When the Federal Reserve (economy) announces changes in interest rates, it will affect the amount of interest a bank will charge for a borrower in the future. Currency markets will have an immediate reaction, as typically the dollar will strengthen (the currency has to be appealing to outside interest) with increases in interest rates. Additionally, stock markets will change stock values based on offering a new discount rate for future earnings. Commodity prices will have indirect implications as well based on the change in the dollar value. The probabilities and actions of one institution will cascade throughout interconnected world markets.

Beginner example:

Think about a bunch of kids on a playground that are playing with a small ball. A couple older kids (adults or institutions) have the ability to kick the ball harder, and further. When they kick the ball, the ball moves either higher or faster out of reach of the smaller kids, and the smaller kids adjust accordingly to follow the direction the older kids send the ball. A market works in a similar fashion. When a big player makes a big decision, the others react accordingly to that change.

Additionally, risk management tools provided by financial institutions stabilize the markets. An institution that offers derivatives such as options and futures allows a company to hedge against the price fluctuations of a currency, commodity, or interest rate. Without the institution as a market maker and a counter party to buy and sell, conditions would be very different and volatility would be much higher.

The macro effect is more than the mere trade of the subject account. The bank, conditional to their lending practices, functions as an availability of credit with respect to the decision of financial risk. When the institution isn't lending credit, the economy slows down, operations or expansions are halted. Too much loose credit speeds up growth of an economy and increases probability for asset bubbles.

Institutions are also providing the physical and technological infrastructure for price discovery. A market maker can continuously post bids and ask prices over a wide variety of asset classes. This ensures that someone is always willing to take the other side of a trade. This operation reduces overall transaction costs while providing a more efficient market.

Trading Platforms & Market Infrastructure Explained

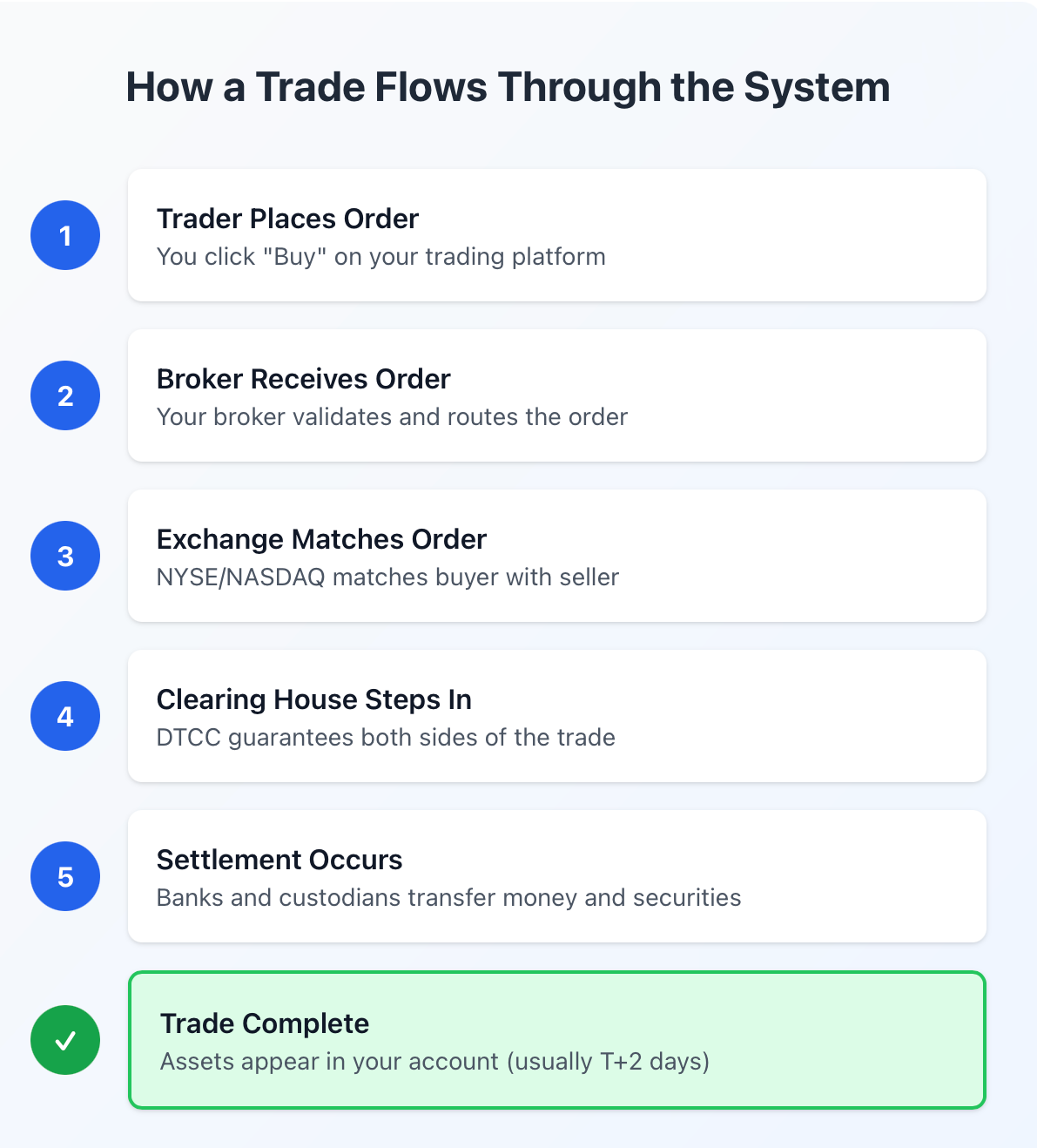

Every trade you complete is supported by an intricate system of institutions coordinating actions that facilitate that trade. Familiarizing yourself with this framework can enhance your appreciation of a system's stability to potentially understand when it stops working.

Most trading occurs on exchanges, which function as places for buying and selling. The New York Stock Exchange operates an auction market with designated market makers who stand ready to buy or sell stock for their own account.

The NASDAQ operates as a dealer network. CME Group is the largest derivatives marketplace in the world, focusing on futures and options, and enabling speculation on pricing in everything from crude oil to bitcoin. These exchanges facilitate trades between buyers and sellers, oversee procedures and rules governing trading activity, provide a means of ensuring fair prices, and add transparency to the pricing in the event of a price discovery process.

Professional Example: For example, CME Group's futures exchange allows an airline to procure fixed fuel prices months in advance by purchasing a crude oil futures contract. This hedging is important because it minimizes the airline's exposure to price spikes in the market, giving the airline budget certainty. In addition to reducing risk to airline budgets, speculators will buy the airline's crude oil futures. In this manner, the speculators play an important role in providing liquidity to the market by providing the opposite side of the crude oil futures contract, ensuring that the futures market has sufficient depth and liquidity.

Beginner Specification: Think of an exchange similar to an exam hall when you were in school, where every student must abide by strict rules regarding when they can enter, how they conduct themselves while taking an exam, and how they submit their exam responses. Your teacher, who was supervising the exam, ensured that no one cheated. The same could be said of an exchange and the compliance monitoring procedure consumers are beholden to follow at the exchange. There are multiple entities established to replace, review and self-regulate the exchange for fair pricing and processing.

Clearing Houses work hard to remain in the background, but are performing critical functions. Once you execute a trade, the clearing house steps into the middle of a transaction as a counterparty to both sides of a transaction.

For example, if you bought 100 shares of stock, the clearing house guarantees you'll get the stock back even if the seller of stock fails to deliver it to you. The role of a clearing house goes beyond this though, as they manage risk altogether through a number of various means, including margin requirements, daily mark-to-markets, and default funds. The Clearing house will utilize positive capital of other clearing members to ensure money flows toward you. It is common for an organization like the Depository Trust & Clearing Corporation (DTCC) to be clearing and settling trillions of dollars in transactions through the clearing house on any given day.

Settlement Banks and Custodians will physically move the money from settlement banks to custodians. When you sell a stock, your money doesn't magically appear in your account. The settlement banks and custodians perform the duty of moving and settling the money for you, and they keep track of related ownership records.

Remember, settlements can only occur if the custodian is on the hook for the stocks traded from the settlement bank to facilitate the stock trade. To reduce risk, custodians are often utilized as branding banks to facilitate monetary payments, such as State Street or BNY Mellon, as part of an institutional asset manager's or similar organization.

Payment Processing influencers such as Visa, MasterCard, and PayPal create the circulatory system of commerce. Each time you swipe a card an extremely high number of organizations support fund distribution, fund verification, fraud checks, and ultimately process settlements between banks. Additionally, these networks are capable of processing thousands of transactions per second, creating the experience we call modern commerce.

Derivatives Trading Platforms have their own versions of the IOB providing access to exchanges to options, futures, CFDs or Contracts for Difference, and/or currencies. Like the IOB labs where borrowing is possible to upgrade potential customer returns through managed leverage outside of fees, carrying large leverage to support trader account minimums creates opportunities for the customer, however leverage can also be estimated as a mini-downturn situation since leverage can be used to amplify profits and losses.

The infrastructure has taken decades to arrive here, efficiently balancing processes and safety. With this in mind, there are multiple layers of redundancy, regulation, and oversight that minimize the chances of market downturns occurring from settlement failures. When you click "buy" on a trading app all of this, combining together, puts tens of thousands of transactions billions of times a day.

Investors' Interaction with Financial Institutions

Your effectiveness as a trader or investor depends, to some extent, on understanding how to navigate the services financial institutions provide. The nature of these relationships is not simply transactional; rather, they are meant to be developed as strategic partnerships that have the potential to expand your capabilities.

Trading Accounts are customized in various forms based on different needs. A cash account allows you to trade the funds you have available, whereas a margin account allows you to borrow funds to exceed your position size. Retirement accounts (such as IRAs) offer tax-deferred growth opportunities but come with restrictions. Knowing which account type meets your needs and aligns with your strategy can help you avoid costly mistakes.

A financial institution can offer various leverage tools that can magnify your returns (and risk). For example, Forex brokers often extend leverage ratios of 50:1 or 100:1, meaning you can hold $100,000 in currency with only $1,000 in margin (your capital contribution). CFD brokers also allow similar leverage ratios for stock, commodity, and index trading. Leverage assists you to amplify your upside on the right trade, but it can decimate accounts within a few minutes if utilized recklessly.

Professional example: Charles Schwab made history in retail investing when it offered zero commission on stock trades, effectively creating an environment where the opportunity to trade more frequently became economically viable for even the smallest investor. The company has a trading platform that includes research tools, pricing quotes, and education resources, effectively democratizing access to markets that have historically been exclusive to the rich.

Beginner example: Using a broker is similar to using resources in a library. You do not have to purchase every investment research report or all market data as the financial institution will provide these services as a part of the relationship. If you were required to pay for these research and tools independently, it could easily cost you thousands of dollars each year.

Market Data and Market Analysis is another important service. Institutions provide Level II quotes that display the order book depth, options chains indicating implied volatility, economic calendars to assess when important data will be released, and analyst reports compiling information on thousands of companies in the public domain. The asymmetrical information advantage historically favored the professionals but now, there are limited retail outlets that provide almost identical information.

Demo Accounts and Virtual Trading can allow new traders to practice without risking capital. Most respected brokers are able to offer paper-based trading platforms that simulate real-world trading conditions. The sandbox offered in this type of trading is very helpful in allowing the trader to test a strategy, become familiar with the trading platform, and build enough confidence to allocate real capital.

Risk Management Services can help you build a portfolio that protects your capital. Traders can use stop-loss orders that automatically exit the position when the loss reaches a pre-specified loss amount to protect a losing trade. Options strategies (such as protective puts) can be utilized as an insurance policy against a downward move. Many investment analysis tools will help assess your portfolio diversity, calculate your portfolio's value-at-risk, and construct a rebalancing strategy.

Research or Strategy Advice is a customized service that varies from institution to institution. A full-service broker may provide advice on your portfolio and manage your portfolio, but the fees for this type of advice are generally higher. A discount broker may offer a do it yourself platform with a library of educational content and provide information about an automated portfolio. A robo-advisor uses a computer algorithm to build and manage a diversified portfolio based on your risk tolerance and goals.

Selecting an institution can be based on a number of criteria, or factors. Of course trading costs are important, but you should also consider how reliable the platform is, how responsive customer service will be, the markets offered, and consideration of regulatory protection to name a few. A low commission brokerage is worth even the amount you will save, if the platform crashes in a moment of high volatility or the institution does not offer the specific instrument that you want to trade.

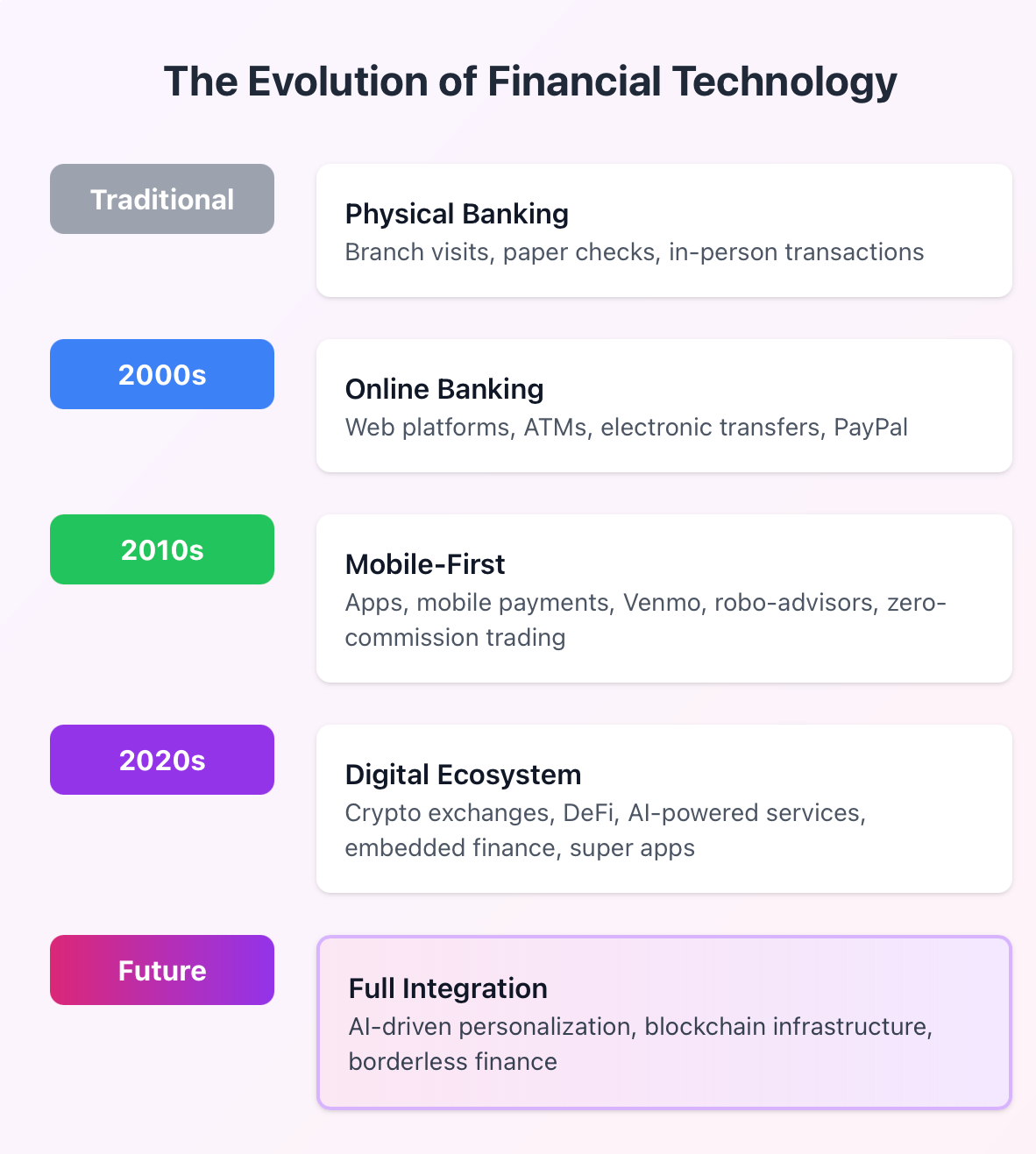

Global Trends & FinTech Impact on Financial Institutions

The finance industry is changing at an accelerated pace driven by technology, regulations, and emerging consumer expectations. If you can get a firm grasp on these trends, you will be positioned to benefit from the next wave of opportunities.

Digital Banking has gone from a potentially-gimmicky app to a known must-have for consumers. Traditional banks are losing customers at an alarming rate to digital-first competitors (such as Revolut, Chime, N26). While traditional banks require ongoing infrastructure and staffing costs, traditional brick-and-mortar banking will have inefficiencies compared to lower-cost, faster, better customer experience, and lower fees of digital-first banks that do not have to incur the same costs of a branch network. Every day we see examples of apps on our mobile phones providing functionalities that we would have been required to go to a bank branch to perform just 5 years ago.

Mobile Payments have surpassed anyone's wildest imagination. PayPal was the first to offer online payments, but services such as Venmo, Cash App, Apple Pay and Google Pay have come to market making it an actual instant peer-on-peer payment, without fees. In most emerging markets mobile money platforms (e.g. M-Pesa) will process more transactions than banks are involved in. The networks are also making the transition from cash to access to financial services for many for the first time.

Cryptocurrencies have created a new type of financial institution. Exchanges such as Coinbase and Kraken, create a common on-ramp to convert traditional currency into digital assets. The exchanges and crypto banks even allow deposits back to clients to earn interest on these digital assets, often at a better rate than traditional checking or savings accounts. For early adopters, decentralized finance (DeFi), is creating a way for consumers to lend, borrow, and trade, without any traditional financial institution to conduct transactions. But risks are also more than with traditional banks, as nearly all intermediaries are removed.

Example: Revolut started as a very simple app to exchange currency at the best rates and has expanded to a full digital financial service competing in dozens of countries. Consumers can hold multiple currencies, trade stocks and cryptocurrency, access credit, and meet day-to-day banking needs within a single app. The convergence of these services is the future of financial institutions.

A beginner-friendly analogy: Mobile banking is akin to a wallet that can be accessed anywhere in the world. Need to pay a friend who lives in another country? You can send the money just like that, while sitting in your room, all through your phone. Want to see your investment portfolio? You can look at it while you are waiting for your coffee. You no longer have to go downtown to visit the bank to do these things – now you can just pull out your phone, wherever you are in the world, at any time of day, and meet your basic banking needs.

Cross-Border Finance is becoming seamless. Services like TransferWise (now Wise) and Revolut undercut the pricing traditional banks use for international transfers by using local banking systems instead of costly correspondent banking networks. This has saved consumers billions of dollars in fees every year to pay bills, send money, and handle other international finance transactions.

Regulatory Evolution determines how a financial institution can operate. Europe's MiFID II improved transparency in the financial markets. Open banking regulations require traditional banks to share customer data (with permission) with third-party apps in order to create competition and innovation – something that has never happened in banking before. Different regulatory bodies around the world are likely to make Know Your Customer (KYC) and Anti-Money Laundering (AML) processes more stringent than they have ever been before when customers want to open an account or when transactions in their accounts need to be monitored.

Artificial Intelligence and Machine Learning are determining how institutions operate. Financial institutions that invest in their digital presence, use AI for fraud detection, or use algorithmic trading methods will become the norm. Institutions that use AI identify customer responses to chatbots, credit scoring, and personalized product recommendations, just like any other industry. AI doesn't just improve efficiency for institutions; it also raises issues of bias, transparency, and loss of jobs.

Sustainable finance will continue to be a growing focus. Much of this is due to ESG (Environmental, Social, Governance) investing transitioning from a niche offering to a more mainstream product offering. Institutions with substantial financial backing, able to invest large sums of money, will start to offer consumers sustainable funds, green bonds, and carbon-neutral banking options. Operational risk will take climate risk into account as standard, just as risk management practices have always done.

For investors, some of these emerging trends will continue to present market opportunities and challenges. Those investors who adapt to and engage with new platforms will gain better returns, more access, and alternative products that aren't available in traditional platforms.

New products in financial markets often have new risks associated with them, particularly in the cryptocurrency and decentralized finance (DeFi) markets where limited regulatory consumer protections exist. When choosing a financial institution, consumers should not just consider their current offerings but also their capacity to adapt amidst continuing evolution.

Conclusion

Financial institutions form the backbone of today's economy, whether you're aware of it or not. Banks are where you save your paychecks, brokers are where you execute your trades, insurance companies are the reason your assets are protected, and central banks are the entities that influence the interest rate, which has an effect on your mortgage. Understanding how financial institutions operate is not only educational, but it's crucial for an individual to make an informed financial decision.

We have summarized the various types of institutions from commercial banks that serve a substantial number of everyday consumers, to investment banks that focus on billion-dollar deals, exchanges that serve as trading venues, and clearing houses that make sure these trades settle appropriately and promptly. Each one of these institutions has a particular and definitive role in the financial system that is woven together across the globe.

Financial institutions impact markets directly and forcefully. Their investment decisions influence prices, their hedging vehicles dampen volatility and their infrastructure facilitates reliable transactions, often instantaneously. As an investor and a trader, your level of success relies on your understanding of this background, and when to choose the right partners.

Technology and financial services are changing rapidly; it is difficult to keep track of how the evolution continues to reshape the steep learning curve. Digital banking and mobile payments, cryptocurrency and blockchain platforms, and services driven by artificial intelligence are making financial markets and services accessible like never before. Technology and digital platforms are reducing barriers to entry, reducing friction, providing cost efficient transactions, and creating tools that were traditionally available only for institutional/ professional trades.

The financial world will continue to evolve, and the underlying principle will remain the same: Agencies that efficiently allocate capital to make investments, diversify risk, and serve the best interest of their clients, will flourish. As a more educated participant in the financial markets, and by understanding how this world works, you will set yourself up for the greatest probability of success.

Ready to act on this information? Visit BTCDana to experience professional trading technology and tools, practice demo accounts and access informative market/ trading analysis, so you can trade forex, stocks and CFDs more comfortably.