The forex and cryptocurrency markets never sleep, and the same goes for those algorithms that quietly earn billions in trading every second. This is quantitative trading, where math and money collide and emotions take a back seat.

What Is Quantitative Trading and Why It Matters in 2025

Quantitative trading (or "quant trading") is defined as the systematic buying and selling of assets using mathematical models, statistical analysis, and algorithmic decision-making. Instead of relying on gut instincts or chart patterns, quant traders let the data dictate every single move.

It's like this: traditional trading is like driving through rush hour traffic and making split-second decisions based on what information you have. Quant trading is like an autopilot that has already evaluated millions of cars and traffic patterns, and knows exactly when to accelerate, brake, or change lanes.

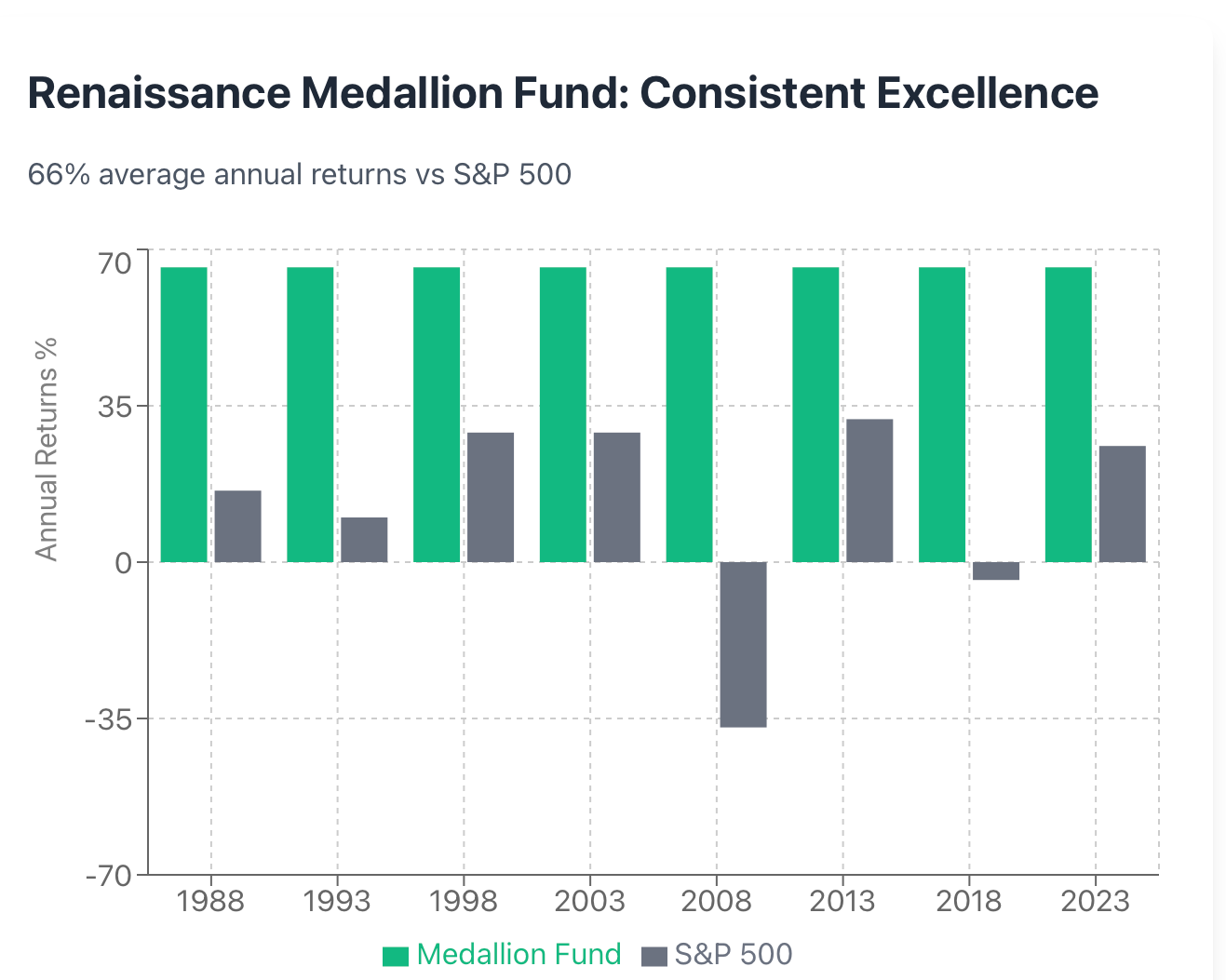

Quantitative began to gain traction on wall street in the 1980s when hedge funds began hiring physicists and mathematicians - who they nicknamed "quants"- to build models. Today, in 2025, quantitative strategies now dominate the global market. Renaissance Technologies' Medallion Fund, perhaps the best-known quant fund in the universe, has been averaging around a remarkable 66% annual returns since 1988; largely, this was attributed to their use of sophisticated mathematical models to spot patterns in the market that human traders couldn't see.

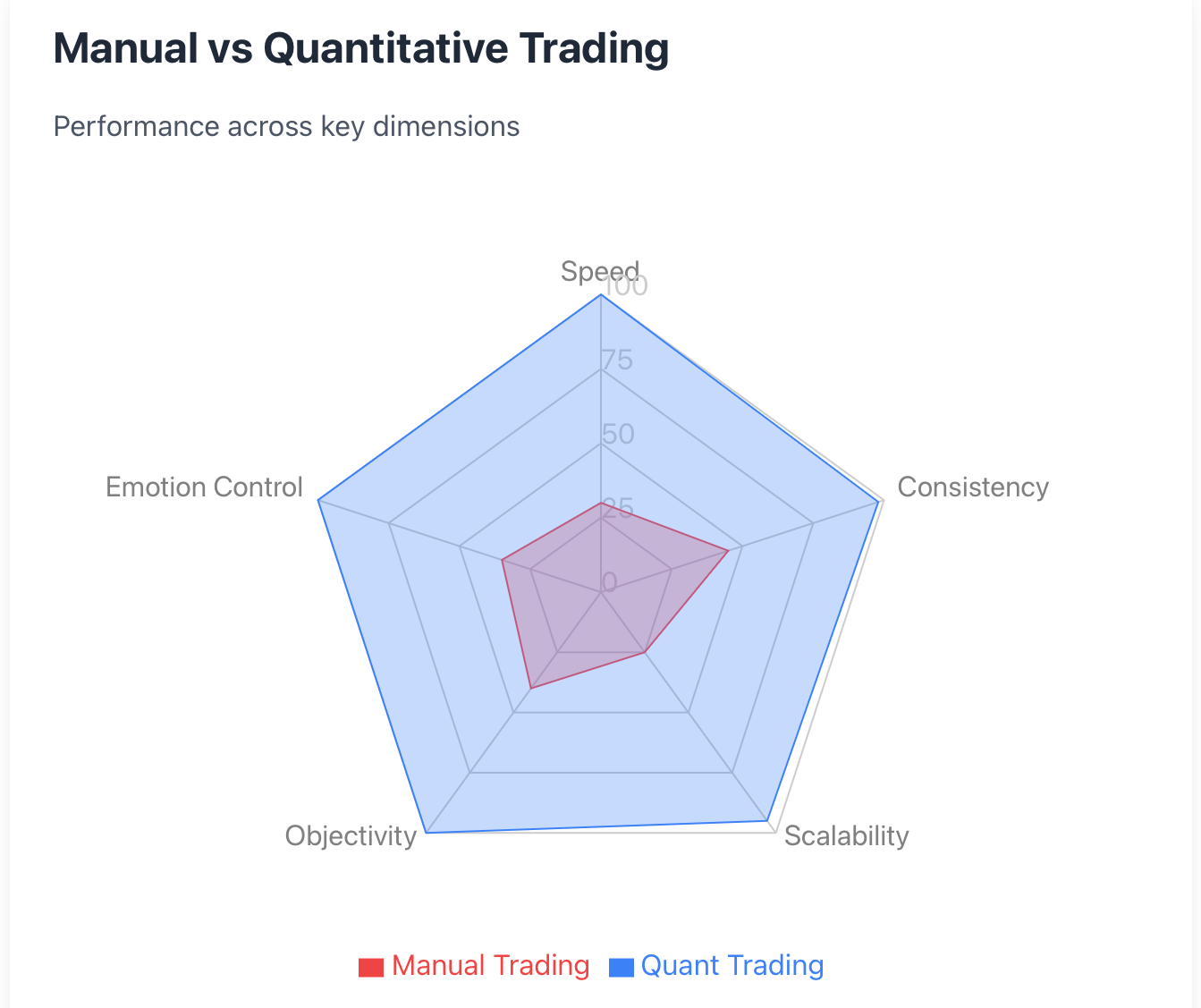

The beauty of quantitative trading is that it is objective. Markets are driven on fear and greed, however, a well-designed algorithm does not panic when market crashes happen nor does it become overconfident when the same comes in a bull market. It simply executes pre-defined rules and statistical probabilities.

Quant trading is not just for billion-dollar hedge funds anymore. Retail traders also have access to tremendously powerful tools like libraries in Python, QuantConnect platforms, even TradingView, with Pine Script, to build their models, and now analyze and assess the performance of their own strategies. The barrier has collapsed, and everyone with the resource of time and the desire to learn can engage in data-driven trading.

Manual vs. Algorithmic Trading

From Wall Street Elites to Your Laptop: The Evolution of Quant Trading

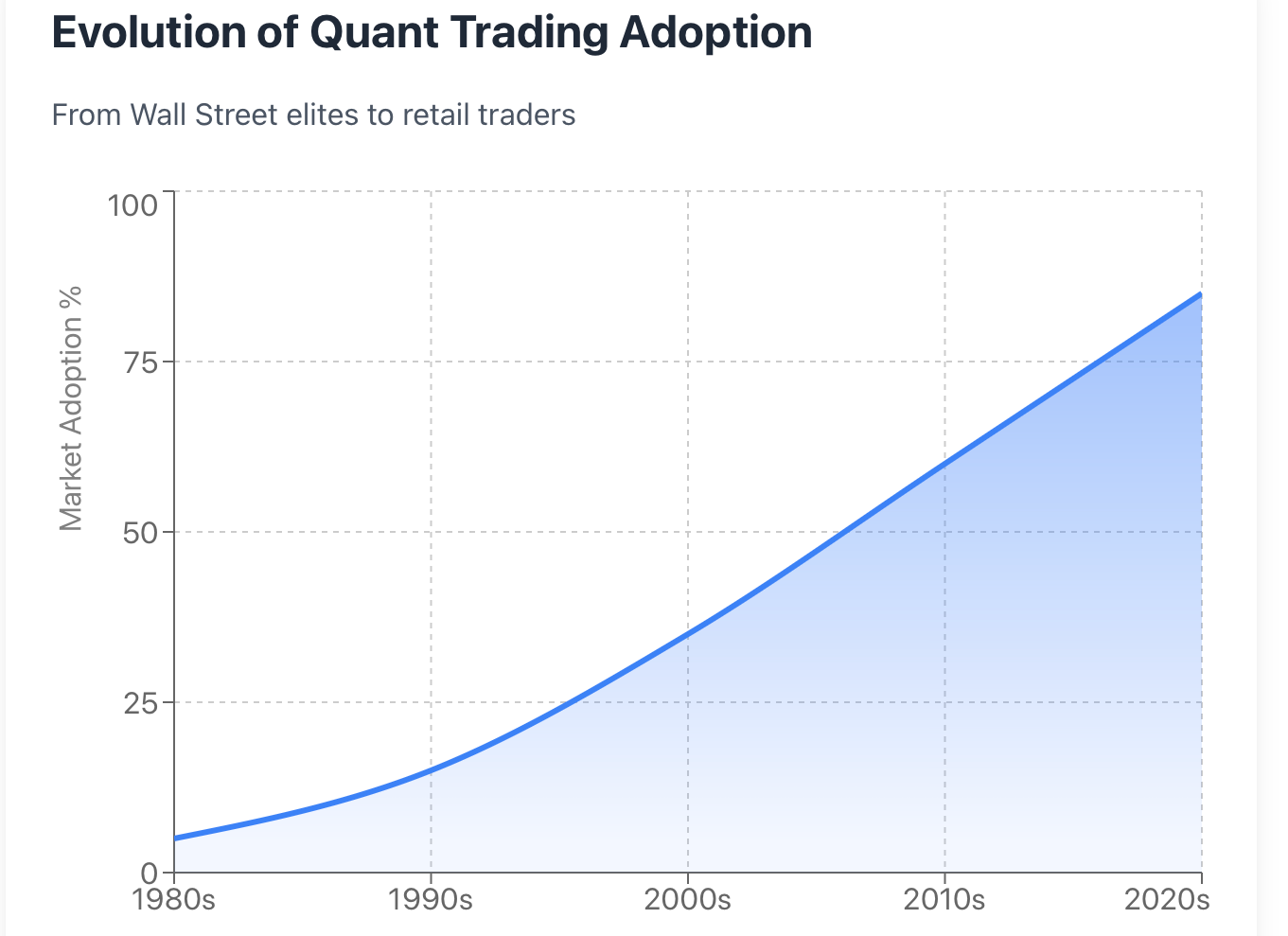

In the 1980s, engaging in quantitative method trading meant one had to have a PhD in Math and be at some institutional trading desk. Early in the quant space, there were firms like D.E. Shaw and Renaissance who had hired academic people who had never thought about the finance dimension.

By the 1990s, computers were getting a lot faster with advanced statistical methods. Pairs trading, which was trading around a relationship between two correlated stocks, became a forerunner to quant trading, and electronic exchanges were replacing the pits (where traders literally were shouting for orders).

Then the decade of the 2000s came and high-frequency trading emerged as quant logic was programmed into businesses to buy/sell within micro seconds. This changed the game as it became more about who had the fastest and most reliable infrastructure and the best connections to the exchange and the best feeds and the most efficient code.

The idea of machine capabilities by quant firms like Citadel and Two Sigma became the "peers" to challenge each other to remove entirely the noise of human involvement by coordinating and sifting through incredibly large datasets to find very tiny inefficiencies that would produce large returns.

Then, by 2020, everything began to change again. Cloud computing, open source machine learning libraries, and commission free trading applications changed quant trading forever. A retail trader in Singapore could suddenly have the same technical capabilities of a hedge fund, without needing a billion dollars of data centers.

Now, there are several key players ultimately divided by continents. In the US, the firms Citadel and Two Sigma are managing tens of billions in quant strategies. In the UK, The Man Group has systematic fund offerings that trade all asset classes (including bonds and commodities) based upon the same systematic premise. And Singapore has become a unique hub for algo-trading as fintech and finance haveThe transition from driving manually to investing with autopilot is done and there is no way back.

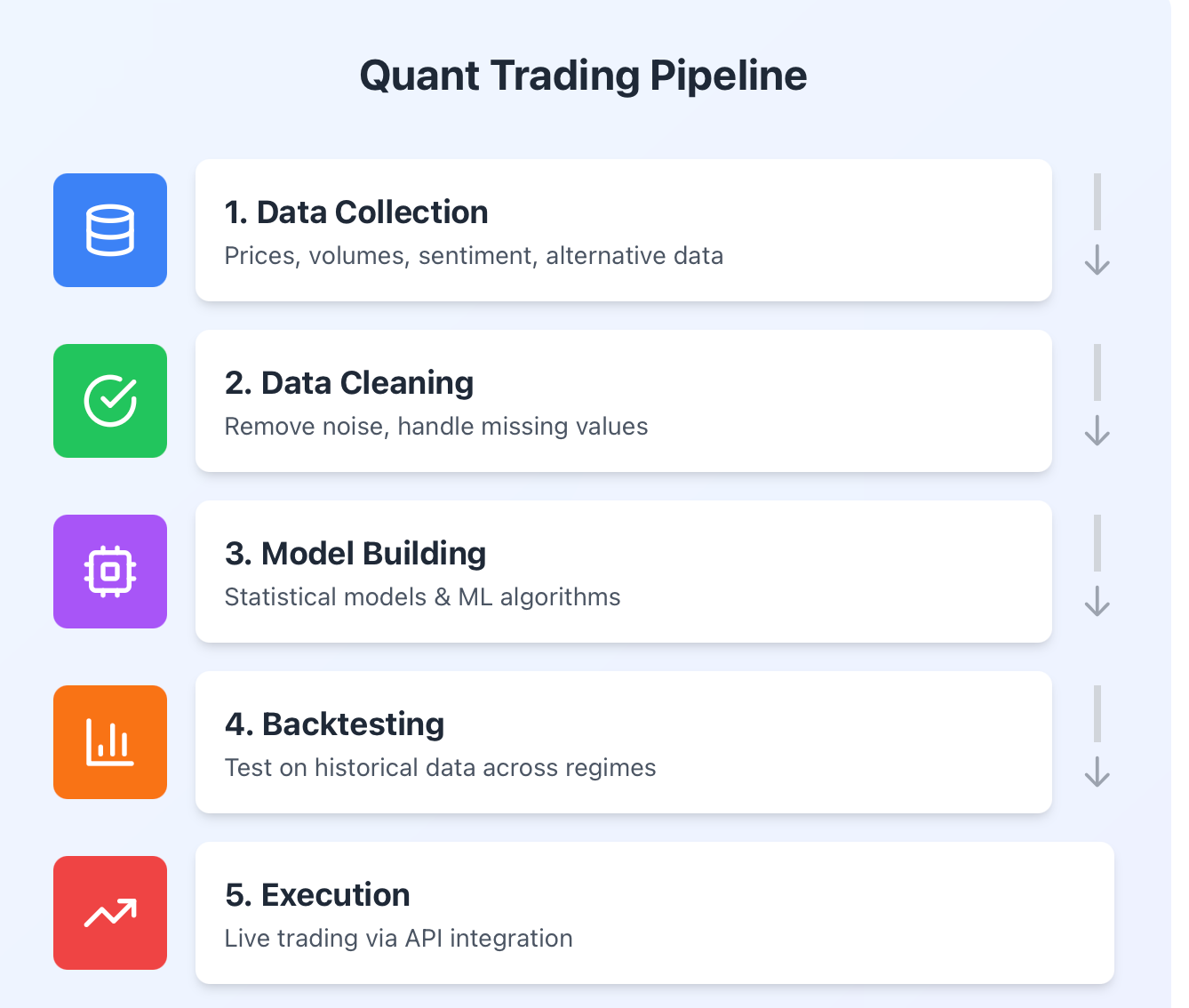

How Quant Trading Works: Full Pipeline

Constructing a quant strategy isn’t voodoo. It’s a systematic practice of converting raw data into auto trading decisions.

1. Data Collection: All of the action starts with data: historical prices, volumes traded, economic indicators, earnings release, Twitter sentiment, maybe even satellite imagery of the retail parking lot. The point is to compile information that has a chance to predict future price movement.

2. Data Cleaning: Raw data is messy. There are missing values, there are outliers caused by flash crash, and there are mistakes made possible by the glitchy exchange. Data cleaning entails eliminating the noise while retaining non-noise that is important. If you skip this step, your model will learn garbage, ultimately it will not be profitable.

3. Model Building: This is where statistics and machine learning become involved. You could either construct a relatively simplistic MA Crossover system or train a neural network to predict vol. The keys to a trading model are the patterns it will find that repeat often enough to be exploitable.

4. Backtesting: Before risking real money, you run your strategy through historical data. Did it actually make money in the volatility of 2020? What about the rate hikes of 2022? Backtesting will help reveal if your edge is really an edge, or just data mined good luck.

5. Execution: If the backtesting is viable, the strategy will go live. The code will interface with a broker through APIs and the scripts will automatically buy/sell when conditions are met. Execution quality is extremely important, as poor execution through slippage or latency kills thin margins.

To help illustrate: A hedge fund might employ a high-frequency arbitrage trading strategy to exploit microsecond difference of price between exchanges, requiring colocated servers with custom-made hardware. A retail trader might use Python to determine which forex pairs tend to revert to mean following a large move and place trades through MT’s API.

The thought process on the whole pipeline is based on one premise: speed and quality of data are determining factors to success. If the feeds for data are slow, then opportunity is lost. If the data is poor, there are false signals. And if execution is sloppy, then profit is lost to fees and slippage.

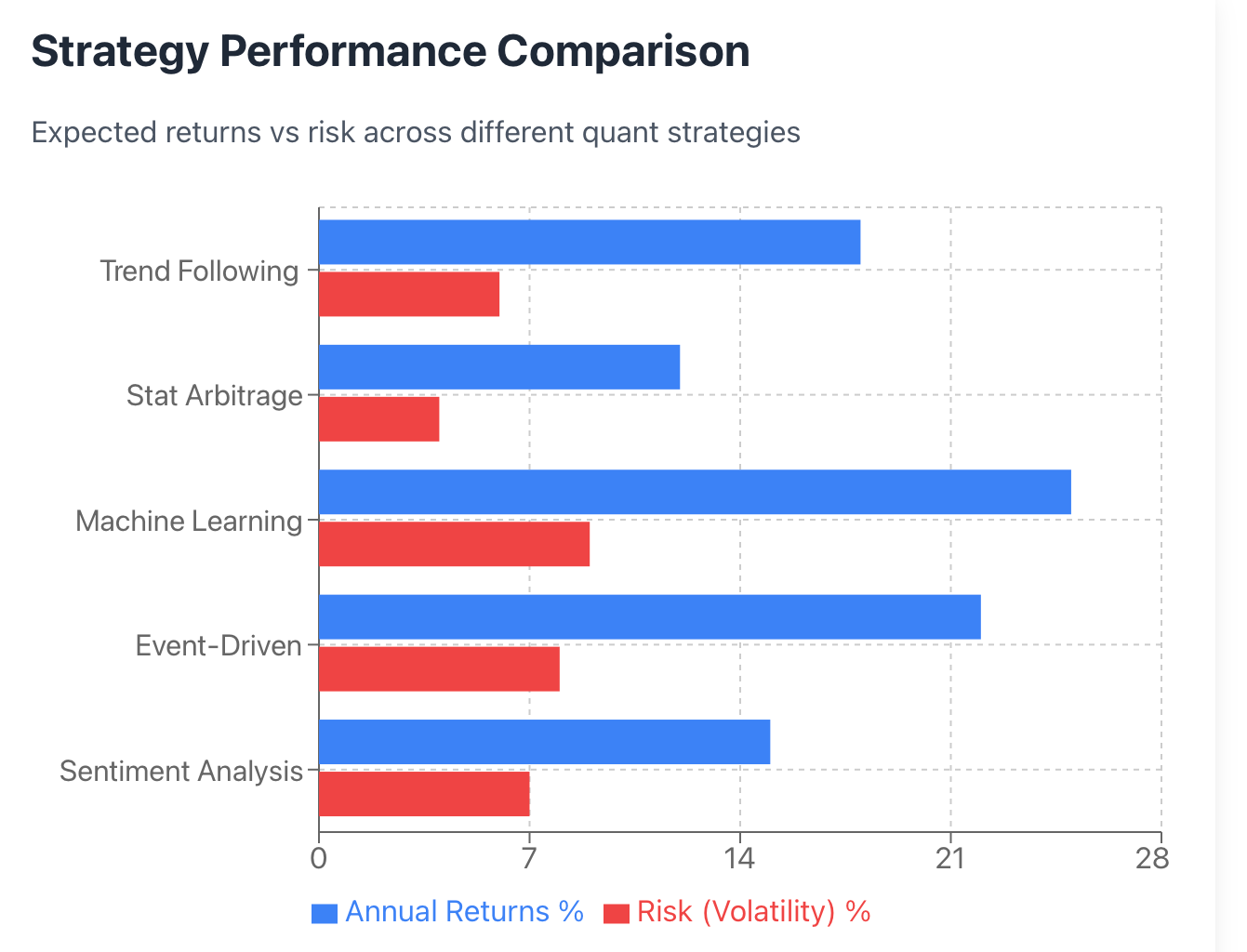

The Main Types of Quant Strategies You Need to Know

Quantitative trading is not a one-size-fits-all discipline. Different strategies leverage different market behaviors, and each has different data and assumptions.

Trend-Following Strategies: This relies on the assumption that things that have gone up will continue to go up (and vice versa). A classic example is the moving average crossover: when the 50-day moving average crosses above the 200-day moving average, buy. Trend-following strategies tend to work well in strong directional markets, but when prices revert and go up and down, they get chopped up.

Statistical Arbitrage: Involves finding pairs of assets that have historically moved in the same direction, and betting that when one diverges it will revert to the mean (converge). For example, if Coca-Cola and Pepsi stocks trade closely together, and then Coke drops, assume that the divergence will eventually converge; to do this, you would buy Coca-Cola short Pepsi and assume that they will close the gap on price. Mean reversion is a part of this family.

Machine Learning Models: Using methods such as neural networks and ensemble methods you can accommodate many different features and learn direction, volatility, or the optimal time to enter a trade. These do well because the models can adapt to changing patterns but the risk of overfitting is always present (it can memorize noise, thinking it has learned a signal). Deep learning has been great at finding the non-linear relationships in increasingly complex functions.

Event-Driven Trading Algorithms designed to aggregate reactions from movements in important identified events such as earnings announcements or the decision from the Federal Reserve or a geopolitical event. The quality is how to absorb that information quicker than human traders can, and to act before the market fixes itself from the information.

Sentiment Analysis: You could gather data from social media using sentiment analysis on Twitter and reddit's WallStreetBets or through headlines. Extreme movement towards fear might suggest new opportunities to buy, while extreme movement towards euphoria might suggest caution as a trader awaits price reversion. Again, the use of natural language processing can help you with this.

For each strategy, something has to be given up. Trend-following will give up accurate entries, higher variance, for better payoffs when it works. Statistical arbitrage will give up any large payoffs for consistency. Machine learning will give up a lot of data and computing resources for flexibility. All will depend on your market (forex, stocks, crypto), time frame, and risk appetite.

Strategy Comparison

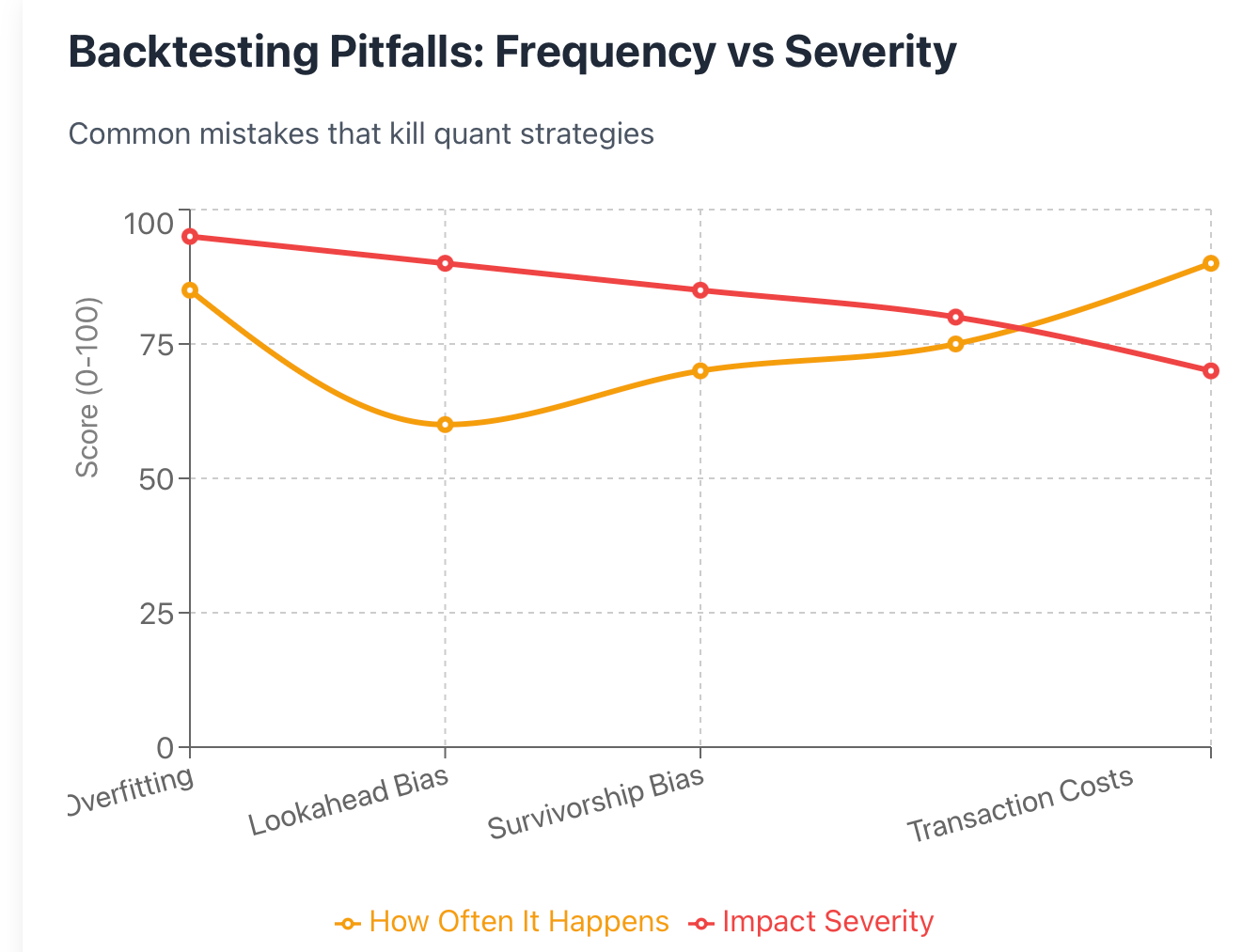

Backtesting: Where Most Quant Strategies Die

You've created a model. It looks great on paper. It is time to backtest it, right? Here is where reality hits you hard.

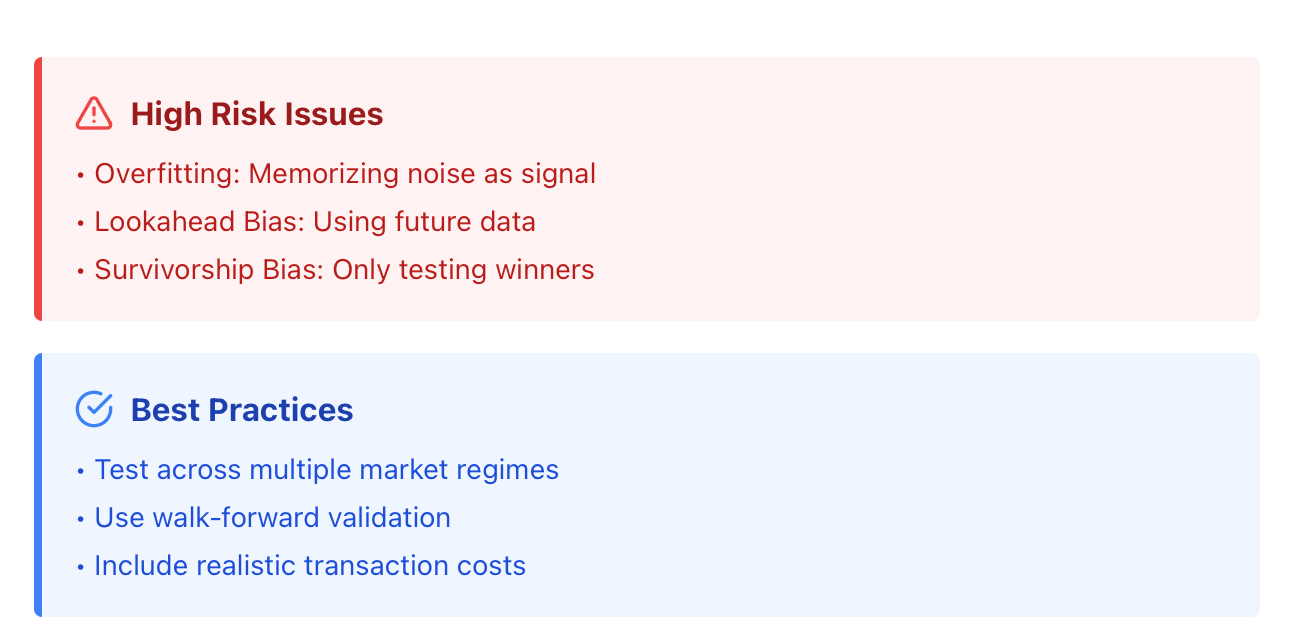

Backtesting examines how your strategy would have performed using historical data. Seems simple, but there are many traps. The death knell of backtesting is called "overfitting". This is when you tweak parameters until the "strategy" can "predict" the past perfectly. Usually, the strategy didn't predict the past perfectly, it just memorized flaws in the market that will not be repeated.

There is also "lookahead bias." This is when you "accidentally" use future information that you would not have known at the time. For example, using a security's closing price at 4 PM to build out models to enter a position at 2 PM. "Voila", you have just generated an illusion of profit.

"Survivorship Bias" is also tricky. If you backtest a stock-picking strategy, you may be using RBC's S&P 500 constituents, which only reflects today's S&P 500 members, completely overlooking companies that have gone bankrupt or have been delisted. Your performance will look great because you are only running a backtest on former survivors.

A good backtest means testing model assumptions across each of the three market regimes (bull, bear, sideways chop), different time-periods, and potentially different parameter settings. If your strategy only works with extremely tight parameters during one specific period, then it is probably worthless.

Take a real example: backtest shows a client annual returns of 40% from 2015-2019. This isn't bad. However, your model fails during first live trading in 2020 when COVID crashes the market and wipes out all of these gains in a matter of weeks. The model has not learned this because the volatility of that environment was not contained in training data.

Good backtests are stress tests for all of your model assumptions. What if the transaction costs double? What if liquidity dries up? What if there is a flash crash? If your model "works" in these environments, there is a chance it may have actually worked in the past.

Big Data: Advantage of Modern Quantitative Trading

Twenty years ago, quantitative models were run based mostly on price data and volume data. Quantitative funds appear to continually look for new alpha generators in more sophisticated ways. Funds are comfortable using satellite images of Chinese factories, credit card transaction logs, as well as using sentiment from social media, etc.

Big Data in trading refers to multidimensional datasets of enormous size and complexity that are processed quickly to find alpha that may not be easily available to competitors. One large advantage of alternative data is it is typically updated continuously, unlike more traditional financial statements provided typically every quarter. Satellite images may show that thousands of cars are parked in a Walmart parking lot the day before earnings. Job postings may indicate expansion plans by the company. Shipping manifests may tell you that the company is caught up in supply chain issues.

Machine learning algorithms like this data complexity. While humans may see noise in the data, algorithms can find subtle correlations. Point72 uses natural language processing technologies to analyze sentiment in earnings call transcripts. Citadel analyzes order flow patterns to predict the stock price the following day.

However, larger datasets are not necessarily better datasets. More data means more noise, more computing costs, and a greater risk of spurious relationships. If the goal is to find real signals, quality filtering and feature engineering are nearly essential. Quality datasets outperform quantity every time.

Data Sources and Market Relevance

The Double-Edged Sword: Advantages and Risks

Quant trading has some compelling advantages. The speed is quite obvious; algorithms execute trades in milliseconds while human traders are still processing whatever information they are trying to digest. Scalability is also important, as a single, well designed system can be keeping track of thousands of different assets across different global markets in parallel, something that is outside the capabilities of discretionary traders.

Objectivity may be the biggest advantage a trader in quant trading can take. The markets punish emotional decisions. Selling into panic at the bottom, FOMO buying at the top, revenge trading after a loss, all quant algorithms avoid this flaw in logic. Algorithms follow the same rules, whether it is a good day or bad.

But the risks in quant trading do exist. One risk is overfitting; this creates a strategy that would have worked perfectly in the past data but does not work in a live trading situation. Changes in the market regime can wipe out a profitable quant with one headline or news story, or change in correlated behavior. The 2020 COVID crash was a massive example of this as many algorithms were created based on patterns of the pre-pandemic world.

There is also the black-box factor. Incredibly complex machine learning made decisions that even we (the developers) could not explain. And when something goes wrong (it will), good luck debugging. You are throwing criteria in and watching to see if you get a better signal.

The 2010 Flash Crash is an example of what happened when algorithms did not work virtually as planned. The Dow Jones lost 1,000 points in a few minutes because there were so many automated sell orders that had cascaded on each other and sent markets in panic. Recently, many quantitative hedge funds were suffering severe pain when correlated behaviors broke down during a market dislocation.

No algorithm is foolproof. The best quant traders build in discretionary adaptability, continually monitoring performance and the market to ensure they are willing to shut out an unproven, and possibly broken strategy. Overconfidence will drain accounts significantly faster than a bad model.

Getting Started: Quant Trading for Retail Traders

Retail traders do not need a PhD or a million-dollar trading infrastructure to get started with quantitative trading. The trader's barrier to entry with quant trading has never been lower.

Getting the Tools for Beginner Quant Traders: Python is dominant and easily the best fit because there are great libraries for all the easy work like pandas (for managing data), NumPy (for doing calculations), and backtrader (to test strategy).

QuantConnect has a cloud-based platform where you never have to manage a single server; you can code, backtest, and deploy your strategies all within the same application. TradingView has a very simple markup language known as Pine Script, where you can visually build and test indicators as well. MetaTrader has automated trading through Expert Advisors (EAs).

What You Really Need to Learn: You first, need to limit programming knowledge initially ( admit you will learn more as needed). You only need enough Python to load the data you want, calculate indicators, and read in simple conditional logic. You need to learn basic stats (mean, standard deviation, correlation, regression). You will need to learn enough about risk management (position sizing, stop-losses, portfolio allocation).

A Beginning Quant Trading System: Choose one market (likely, EUR/USD forex). Download historical data. Program a simple moving average crossover model for entries and exits based on the crossover of the two moving averages. Run the backtest on the last 5 years worth of data. Gather the results for the backtest: the total returns, the maximum drawdown, and the total win rate. The most important result is to figure out why you met your expected results or why you did not.

Common Mistakes Learners Make: The first mistake is running a strategy that is too complicated. The second is curve-fitting parameters into the strategy. The third is not taking commission fees (transaction costs) into consideration. The fourth is not thinking it's going to be hard to replicate a backtest in a live execution, which it is. The fifth is risking too much capital before the strategy is proven to work.

The distinction between beginner quant trader learning and being a profitable quant trader will take time; you will have to test, fail, and then learn constantly for the first few years. Be disciplined and methodical; you'll eventually learn better systems than the next guy.

The Future: Where Quant Trading Is Heading

The upcoming decade will fundamentally change the boundaries between AI and trader beyond current recognition. Reinforcement learning, in which models learn optimal trading policies on sample market data through trial and error is becoming mainstream. This will enable systems to adapt in real-time, and no longer just conduct in a rule-based manner.

Aspects of DeFi and crypto also introduce unique opportunities. On-chain data introduces a level of transparency that is impossible in a traditional marketplace. Smart contracts can be used to execute complex strategies automatically based on certain conditions set on blockchain. Cross-chain arbitrage, liquidity pool optimization, algorithmic market making and parameterisation of existing strategies is just getting started.

Regulation will become much tighter. And jurisdictions across the globe will be considering the issues of how to regulate AI driven trading. Issues relating to whether the technology will facilitate market manipulation, systemic risk, and fairness will not fade away. Expect licensing requirements and mandatory risk controls.

By 2030 we may have fully autonomous quant ecosystems in markets. Algorithms will price data, produce hypotheses, backtest strategies, allocate capital, adapt to feedback loops and more without human involvement. The role of human trader may shift more to oversight and strategic direction as opposed to execution.

The technology is ready - the question is not when AI will revolutionize trading but how quickly the revolution occurs and who will adapt first.

Is Quant Trading Right for You ?

Quantitative trading expresses a complete departure from intuition, emotion, art and into data, algorithms, and science. Quant trading has advantages over traditional manual trading regarding speed, consistency and scale.

However, it's not easy. Miles will be spent on technical and statistical competence, and simply being disciplined. Expect to be spending far more time cleaning data and debugging back-tested strategies, than watching chart patterns. Strategies could stop working overnight after working yesterday. There's no magical road map to profits.

The opportunity is very real. Markets generate enormous amounts of exploitable inefficiencies on a daily basis. It is easier and less expensive than it has ever been to leverage technology to capture the opportunities. Whether you are going to back-test mean reversion strategies or build a neural network to forecast volatility, you have to start with researching, learning, testing and adapting.

Certainly start with smaller projects. Before you build a portfolio, thoroughly test one strategy. Expect to learn little when you fail and ignore the price of making mistakes. More importantly, plan to never risk more than you could afford to lose as you figure all this out.

Markets reward those that exhibit rigorous and analytical processes followed by disciplined execution. If you’re ready to start trading smarter, not harder, then your journey into algorithmic trading begins now. Step into BTC Dana and access the very best in trading tools and join the thousands who are already using data to trade the global markets confidently.