Understanding Liquidity Providers in CFD Trading

If you've ever been curious as to why your CFD trades get filled in milliseconds or why the spreads are different between brokers, it's because of Liquidity Providers (LPs). These are the institutions and companies behind the scenes that make sure your order is filled in a timely and efficient manner.

You can think of an LP as the intermediary between your broker and the marketplace. When you are executing a trade on EUR/USD or Gold CFDs, your broker did not magically generate those prices. They are receiving continuous bids and ask prices from the LPs; usually these are large banks or financial institutions. Without LPs, your orders may simply not get filled, or worse, get filled at prices much different than anticipated.

You may be asking yourself, why should I care about LPs? There are two main reasons - cost and experience. The quality of the LP is what determines the spread you pay (the difference between your buy and sell price) and how "quickly" your trades get executed. Brokers connected to higher-quality LPs can offer lower spreads and faster execution. Both of these factors will save you money and headache when entering and exiting your positions.

Let me give you an example using a less complicated story. Let's say you walk into a supermarket to buy milk. If the shelves are full of milk (high liquidity), you grab the carton and checkout without delay. If there is only 1 carton left (low liquidity), you may wait for someone to uncover it or, in the worst case, you may leave without it. Liquidity Providers are the equivalent of the supermarket or supplier providing the milk on the shelf.

From a more professional standpoint, let's think about liquidity for the EUR/USD market being provided by top banks in the world such as Citibank, JP Morgan, or Goldman Sachs. They are constantly quoting prices and taking millions of trades a day, all so your retail broker can offer you instant execution on your $100 trade. The institutional liquidity is being passed down to you as a retail trader.

Basic trading chain looks like this: You (Trader) ↔ Your Broker ↔ Liquidity Provider ↔ Worldwide Market. By understanding the trading chain you can determine which brokers to use and what type of trading conditions you can expect. The better the LP, the better your trading conditions will be.

What is a Liquidity Provider? Definition and Role

Essentially, a Liquidity Provider (LP) is any trader who provides buy and sell quotes into the market such that there will always be someone willing to accept the other side of your trade. In CFD trading, LPs usually refer to the banks, or financial institutions, or specialist market makers who offer brokers two-sided continuous prices to quote to their clients.

So, what do Liquidity Providers do?

They provide bid and ask prices: The LPs are always changing the price for the instrument they support; for example, currency pairs, indices, commodities, and cryptocurrencies. So, if you see a quote on the EUR/USD at 1.0850/1.0852, that price quote is coming from an LP.

They provide market depth: Good LPs will ensure that there is adequate volume behind their quoted prices so that your order doesn't move the price massively. This is important for larger traders needing to place larger positions without experiencing slippage.

They help brokers manage spreads: Part of the quoted spread (difference between the bid and ask) is set by the LPs quote. Brokers can pass on the lower spread to their clients if they can access LPs that provide possible better prices.

Let's look at a few examples to illustrate the difference. Professionally, when a large bank is providing the EUR/USD liquidity, they may quote a spread of just 0.2 to 0.5 pips. The minimal spread is a result of trading at a large volume and at very efficient rates by the banks. Then the retail broker adds a small markup, and the spread on your broker's trading page may show spreads ranging from 0.8 to 1.2 pips.

Imagine being a new customer trying to purchase the latest gaming console during the initial launch of the product. If the LP has sufficient product and your nearby retailer has a dependable supply chain, the retail stores will sell it to customers and you won't experience delays. If the LP doesn't have enough product, or there was a delay getting the product to market, customers will face limited inventory, higher prices, or even no availability. The same concept is true while trading, LPs are the suppliers who fill the order you place with your broker.

Like all things in the financial industry, it is important to make a distinction. LPs are not to be confused with brokers. Brokers are your first and primary contact. They are the platform where you execute your trades. LPs are behind the scenes and are not linked to individual retail traders, they supply brokers. LPs will not be your first contact but the quality of LPs will affect many inputs including spreads and execution speed.

When a broker states that it has "institutional-grade liquidity" or "Tier 1 bank connections," they are implying they are working with a high-quality LP. This implies that they will provide better prices, quicker fills, and less slippage than brokers that use lower-tier liquidity providers.

Liquidity Providers represent the infrastructure of CFD trading; they let you trade 24/5 on the Forex markets or execute a Gold CFD trade at 3 AM. Without liquidity providers, retail trading would not exist in its current form.

Types of Liquidity Providers: All LP Models in the CFD Markets

Not every Liquidity Provider is created equal, and knowing the different types of liquidity available can help you assess your broker's trade execution quality and help you select platforms which suit your trading style.

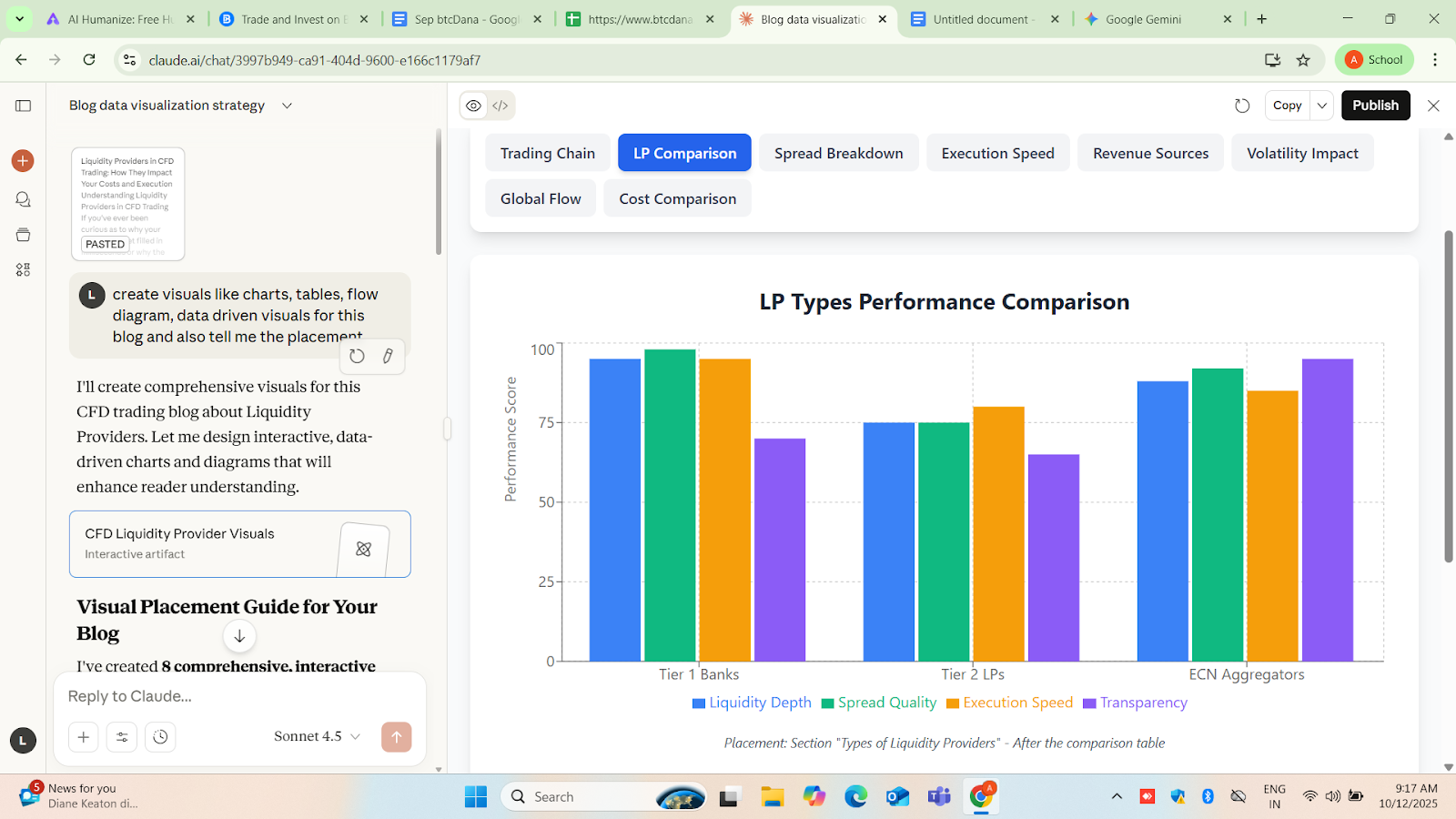

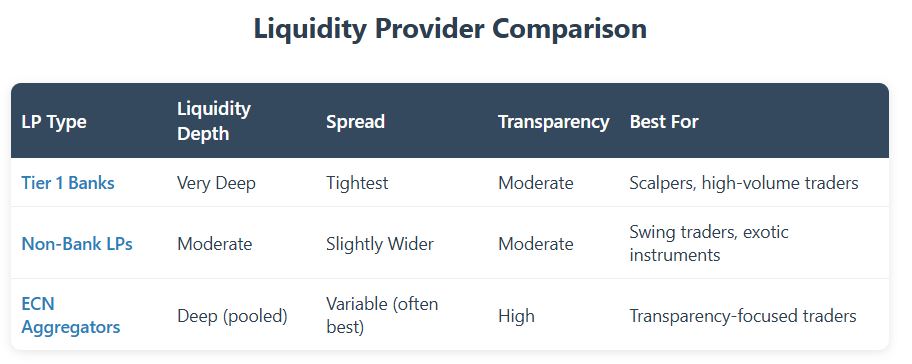

Bank LP's (Tier 1 banks)

These are the biggest players in the liquidity space of big international banks such as Citibank, JPMorgan Chase, Deutsche Bank, Barclays, and HSBC. They offer the deepest liquidity pools and most competitive quotes as they trade huge trading volumes across global markets.

Pros: Extremely tight spreads, strong quote stability, minimal slippage during volatile periods, etc. You are getting institutional-style pricing if you are trading a major pair such as EUR/USD or GBP/USD from a broker who is connected to tier 1 banks.

Disadvantages: These banks usually deal only with established brokers that can meet professional capital and volume requirements, which means that smaller brokers may not have access to that level of liquidity.

Best for: Scalpers, high-frequency traders, or anyone trading big size and looking for the absolute tightest spreads and execution.

Non-Banks LPs (Tier 2 Banks or Marketmakers)

These are smaller regional banks, hedge funds, or trading firms providing liquidity as market makers. They fill the gap left by the Tier 1 banks, often providing liquidity to more exotic pairs, smaller indices, or cryptocurrency CFDs.

Advantages: More flexible relationships with brokers and more likely to provide quotes for less liquid instruments: and can be more accessible than Tier 1 banks for newer or smaller brokers to work with.

Disadvantages: Spreads may be a bit wider than Tier 1 banks and would have less stable quotes, or greater slippage, when there is a lot of volatility.

Best for: Swing traders, position traders, or traders looking to trade less popular instruments that the Tier 1 banks might not be providing models for.

Electronic Liquidity Providers (ECN/Aggregators)

ECN, an abbreviation for Electronic Communication Network, is a platform that pulls quotes from multiple LPs, both Tier 1 and Tier 2, and automatically selects the best available bid and ask price for each trade. You can consider it as a meta-provider which aggregates liquidity from other providers.

Advantages: Maximum transparency since you can often see the depth of market as well as where the quotes were coming from, potentially the tightest spreads since the system will pull the best price quote from all LPs connected, and instead of the LP taking the other side, there will be less conflict of interest as the idea of the ECN is to match orders.

Disadvantages: Often involves a commission albeit in addition to the spread markup as well, and prices can be 'thin' even though the liquidity is aggregated during extreme volatility, and or news events.

Best for: Experienced traders who pay for fairness and transparency; enjoy an execution that is similar to institutions who are aware that prices may vary due to commission and retain some risk versus liquidity price.

Brokers such as IG and Pepperstone frequently boast about access to many Tier 1 banks and ECN aggregators. This access provides them with deep liquidity pools and they gain the benefit of providing extremely competitive spreads and execution to their clients. If you ever see a broker provide EUR/USD spreads from 0.6 pips with no dealing desk, it is because they have a strong relationship with their LPs.

For novice traders, you can think of an ECN aggregator in very simplistic terms as a price comparison website (similar to Booking.com). When you are trying to compare flight tickets, the price comparison to a variety of airlines will give you the cheapest option. In a similar fashion, an ECN liquidity aggregator will aggregate trading quotes and show your broker the best available price in their books.

The type of LP will have a direct correlation to the viability of your trading strategy. If you are scalping, and requiring ultra-tight spreads, you will have to use a broker with Tier 1 bank liquidity. If you are swing trading and holding positions for days, then a slightly wider spread from Tier 2 LP's will not impact your results. Conversely, if you are looking to know exactly where your orders are going to be filled to and from which LPs, then ECN platforms will provide this transparency.

By understanding LP types, you can ask better questions when evaluating brokers: "Which LPs do you connect to and are they Tier 1 banks?" or "Is it an ECN model?" These questions can, of course, tell you a lot about execution quality.

How do Liquidity Providers make money?

It’s necessary to recognize that liquidity providers aren't running a charity. These are businesses that have to be profitable, and by understanding how LPs make money, you can see how trading costs are structured and why spreads even exist in the first place.

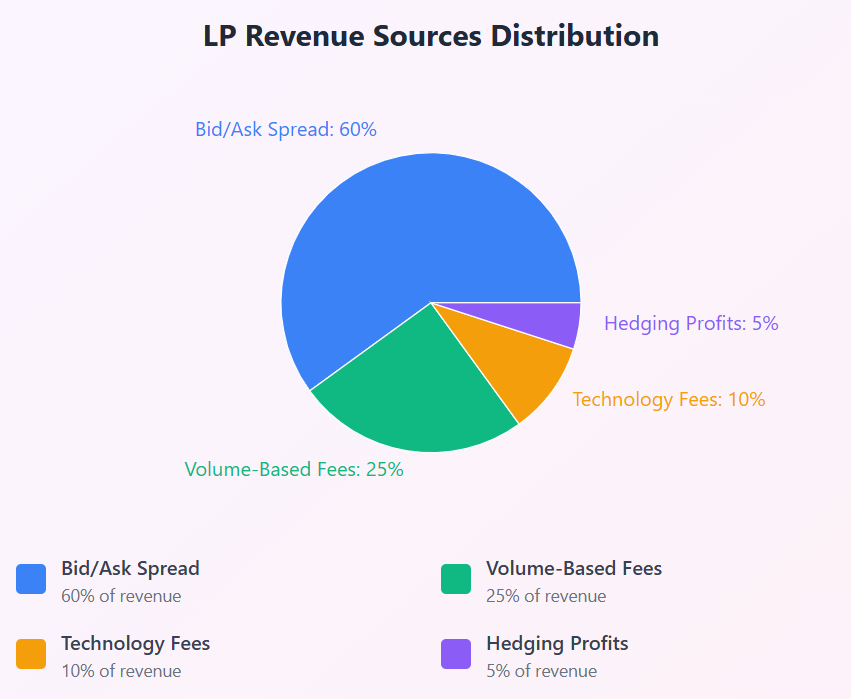

The Bid/Ask Spread

This is the most direct/obvious means of how liquidity providers make money. The spread refers to the difference between the price that the LP is willing to buy (bid) and the price that they are willing to sell (ask) an instrument. For example, if you see an LP quote EUR/USD at 1.0850 bid and 1.0852 ask; that 2-pip spread is essentially their profit margin.

When you execute that trade, you are either buying at the ask price which is slightly higher than the bid, or you are selling at a price that is slightly lower than the bid. The tiny difference is where the LP captures their revenue. When you multiply that by millions of trades that happen daily, it adds up.

For instance, a Tier 1 bank could quote you EUR/USD with a 0.2-pip spread, which is their markup. Your broker will then add another markup for themselves of about 0.4-0.6 pips to account for their costs and profit, and that is how you end up seeing a 0.8-pip spread on your brokers platform.

To help understand the concept of spreads, think about a currency exchange at the airport - you will see that they buy your US dollars at a lower price than you will pay them to buy euros . That difference is their profit; that is the same way LP spreads function.

Liquidity Contracts with Brokers

Many LPs actually have formal agreements with brokers and charge fees based upon volume traded, or require a minimum amount of volume traded to stay an LP. These contracts can be:

Flat fees per month: The broker pays a predetermined fee for the LP to get access to its pricing feed and execution platform.

Fees based on trading volume: The LP charges based on the per million dollars traded, similar to a wholesaler pricing system. Higher volume items usually have better pricing.

Technology fees: Some LPs will charge for API access, connectivity infrastructure or specialty trading tools they provide to brokers.

These expenses ultimately become part of the broker's cost structure, which informs the prices available to clients. If a broker is paying the LP a premium to be the top tier of liquidity, the costs have to be recouped in some way, either through slightly wider spreads as mentioned above or by way of some commission charge.

Market Hedging and Proprietary Trading

The larger bank LPs are typically always hedging their exposure to the market by taking offsetting positions in the actual market. For instance, when the LP is providing prices on EUR/USD to brokers and builds a net long position on the balances, they will hedge their position by selling EUR/USD in the interbank market. The difference between the quoted spread to the broker and the execution price with the interbank becomes their profit.

Some LPs may, on occasion, be active in proprietary trading, meaning the LP has used the market making infrastructure and flow of information available to them to trade as a principal on their own behalf. While this is also separate from providing liquidity as discussed in the role of LPs, it is done using the same market infrastructure and access to the marketplace.

Example: A bank acting as an LP on EUR/USD may notice strong buying pressure at a certain price level. The LP gains access to this information and at the same time may conduct their own independent analysis of the market. The LP may then take its proprietary long position and if the market moves in their direction, the LP will profit.

How This Affects Your Trading Costs

The LP profit model is directly tied to what you pay as a trader. The smaller the spread, the less the LP is making on each trade, and the only way to operate sustainably is at high volume. This is why Tier 1 banks can offer 0.5 pip spreads, they have enormous order flow that allows them to make these small margins per trade profitably.

On the other hand, if you are trading an exotic pair or cryptocurrency CFD where liquidity is limited, LPs need to widen their spread in order to protect against the additional risk and lack of volume. This is not greed; this is economics.

This knowledge is valuable for assessing broker marketing claims. If a broker advertises "spreads starting at 0.0 pips," they are likely presenting you with a razor-thin LP spread and instead charging you a commission for every trade. The end result is likely the same in cost to you whether you are paying a 1 pip spread with no commission or a spread starting at 0 with a commission charged for every trade--it simply is represented differently.

Here's a simple breakdown:

Imagine ECN platforms displaying different LP quotes side by side. You might see a LP stating its quote for EUR/USD at 1.0850/1.0852 (a 2-pip spread), while another LP might give a quote of 1.0849/1.0853 (a 4-pip spread). The platform will send your order to the one with the 2 pip spread, which is less expensive for you. This is how transparency works for you.

The takeaway: LP profit models aren't necessarily bad. They're part of what enables this ecosystem to function. The right LP's and brokers provide a mechanism for saying, 'here is my cost to do business', but do it in a way that is competitively priced for clients.

Choosing a Reliable Liquidity Provider: A Selection Guide

Most retail traders do not directly select liquidity providers - this is the broker's responsibility. Understanding the components of a liquidity provider helps you assess brokers in a better way and facilitates asking the right questions prior to opening an account.

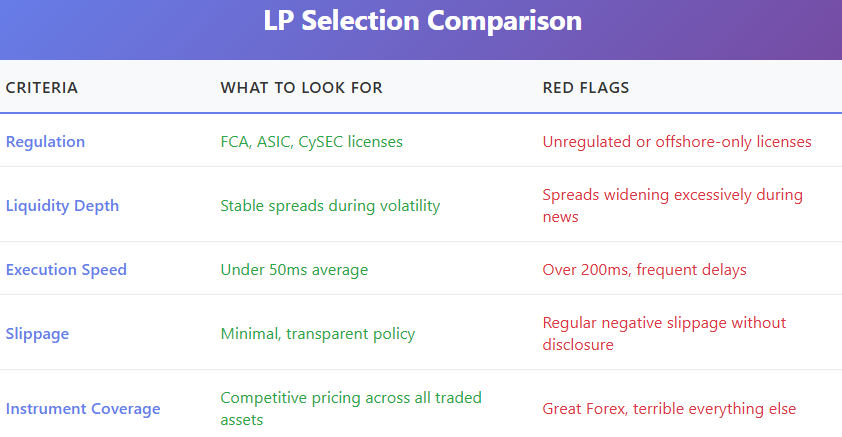

Regulatory Aspect

A good liquidity provider operates under strict financial regulations. Look for a provider licensed in an established financial authority (e.g FCA - UK, ASIC- Australia, CySec - Cyprus, or equivalent). Regulations force the LP to maintain adequate capital reserves, transparent pricing, and segregate client funds.

Why it is important: If your broker utilizes unregulated, or loosely regulated LPs, you're exposed to counterparty risk. The LP could unfairly widen spreads during volatile periods, engage in price manipulation, or potentially go bankrupt.

What to check: Ask your broker which LPs they partner with and research the regulations of those firms. Reputable brokers will publicly disclose their liquidity partners.

Liquidity Depth & Quote Stability

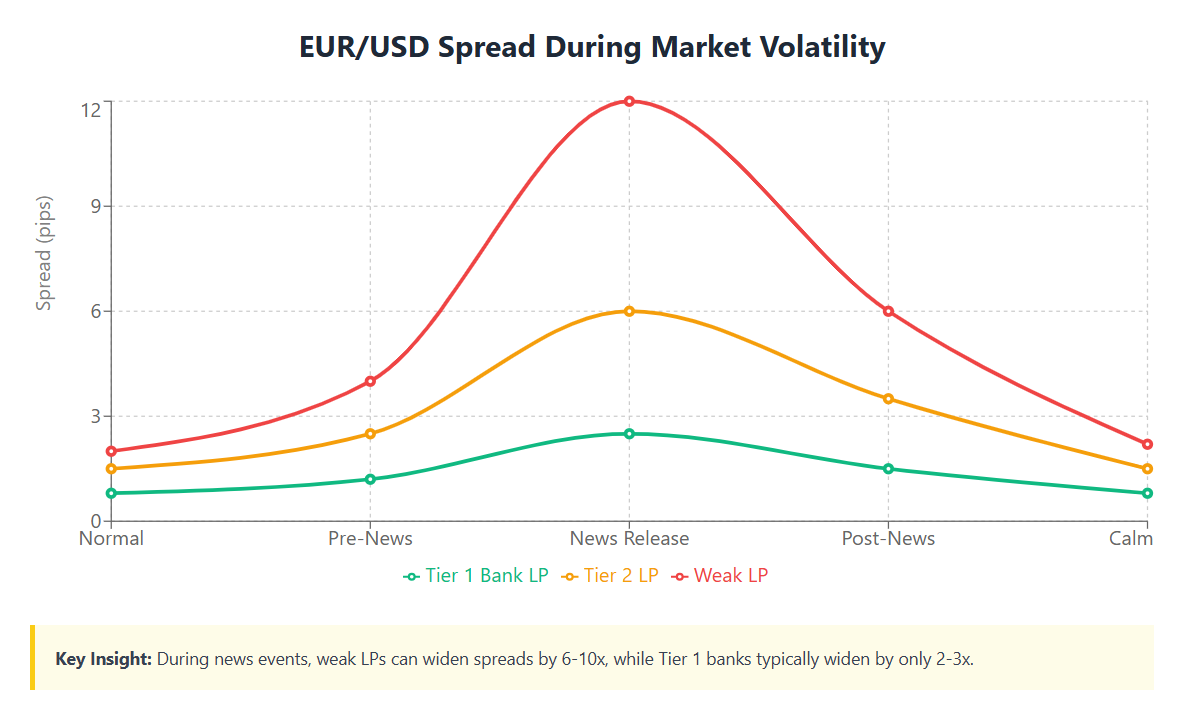

Deep liquidity means the LP can handle a large influx of orders, without significant price movement. Therefore, you will be provided with stable quotes with little slippage during typical trading, however, once we see volatility (like during major news releases) this matters even more.

Why this is important: Lack of liquidity will result in slippage, requotes, and frustrating delays in execution. If you are trading in a fast-moving market, and your order gets filled 5 pips away from your intended entry price, this is most likely a lack of liquidity issue.

What to check: If possible, test the broker out during periods of high volatility on a demo account. When real market events happen (like NFP, or central bank decisions) you can see if the quotes would hold value at all. If pricing can stay stable during noted stress, it is a sign of a well-supported LP.

Example: A broker affiliated with multiple Tier 1 banks might display EUR/USD spreads of 0.8 pips in the calmest of markets and 2-3 pips during extreme volatility. A broker with weaker LP relationships might typically display 1.5 pips in normal conditions and then spiked to 10+ pips during the news. That's a big difference if you're an active trader.

Execution Speed and Slippage Control

Fast execution means your orders get filled at or very close to the price that you see on screen. Slippage is what happens if there's a delay between when you click "buy/sell" and when the order actually gets executed. Slippage means that you actually executed at a worse price.

Why does it matter: Slippage means reduced profitability, especially for scalpers and day traders who thrive on tight spreads and quick in-and-out trades. Swing traders can still feel the pain if slippage occurs regularly in the other direction.

What do you want to check: Look for the average execution speed (usually the broker will indicate this number in the "ms," or milliseconds). Anything less than 50ms is outstanding. Look into their slippage policy, do they guarantee that you'll receive the executed price it displays, or do they usually incur slippage every time?

Example: Two brokers publish EUR/USD quotes with USD 0.8-pip spreads (a very low spread). Broker A can execute the transaction in 30ms and has almost no slippage. Broker B can execute the transaction in 200ms with slippage of 1-2 pips almost every time. Therefore, your effective cost with broker B is 2-3 pips per trade. Broker B will then almost be 2-3 pips *more* expensive than broker A even though they are advertising the same "spreads" on their quotes.

Supported Trading Instruments

Some LPs will excel in Forex, while others are more effective indices, commodities or cryptocurrency CFDs. If you will be trading more than one asset class, check that your broker's LPs are offering you comparable pricing for all of them.

Why this is important: A broker may have excellent Forex liquidity, but if they do not have dedicated crypto LPs, they may have a terrible cryptocurrency spread. You want an LQ that provides you with similar quality in all of your trading interests.

What to look for: Quality of spreads and execution for all instruments you will be trading. Don't just check for spreads on majors in Forex if you are trading Gold, oil or Bitcoin CFDs, for example.

Practical Testing Advice

It's not enough to just take a broker's word for LP quality. You should test it out yourself:

1. Open a demo account: Most brokers will offer unlimited access to a demo account where you can test out the execution of a live trade without concern of actual money being lost.

2. Trade during periods of volatility: Place trades during periods of significant economic releases. This will demonstrate what the LP quality is like under some stress.

3. Compare multiple brokers at once: If you have opened demo accounts with 2-3 brokers, execute the same trades at the same time and compare them. Compare the fills, slippage, and the spreads directly across the different brokers you are testing out.

4. Ask about your execution: Some brokers offer trade execution reports that detail the execution for your trades along with which LP filled the order and at what price. This type of transparency shows confidence in the source of liquidity they are providing.

For example, IG, Pepperstone, and XM all promote multi-LP setups that include access to Tier 1 banks. If you were to open demo accounts with each broker and take the same trades during a Federal Reserve announcement, you would clearly determine which broker is actually doing what they say in terms of spreads and fast fills under the pressure of volatility.

Think of it in terms of determining a mobile phone plan. Service and price are important, but so too is the quality of the network. You wouldn't choose the cheapest service if your phone continuously drops calls. This analogy carries forward to how you should think about LPs, don't focus only on low spreads if you are unsure about the quality of execution.

The objective is to identify a broker that has LP relationships that allow for steady and fair pricing and reliable execution. That combination is much more important than attempting to obtain the highest possible execution on an advertised spread

Liquidity Providers and the Global CFD Market

Liquidity Providers do not only allow individual trades to execute but also facilitate retail traders access to global CFD markets, eliminating the exclusivity that has traditionally belonged to institutional traders.

Connecting Retail Traders to Global Markets

Before LP infrastructure existed, retail traders had limited options. You could have a stock broker purchase stocks for you, or buy a futures contract with a significant amount of capital, or very poor execution via simple Forex platforms. LPs created the bridge between retail brokers and institutional markets, changing the landscape entirely.

When you are trading a DAX 40 CFD from your balcony in India, or a Gold CFD from Brazil, you are trading against liquidity pools that are made available from significant institutions, located in London, New York, or Tokyo. The LP collects those institutional quotes and shares it in scale with your retail broker. Without LP infrastructure in place, you would be required to have access to capital in the millions, plus direct access to the market, to even trade these instruments.

For instance, if an individual makes a trade in Dubai through a trader and a broker connected to high-quality LPs, they will receive quotes that are based on and informed by the actual pricing in the futures market. The trades can be executed in seconds and are accessible with or without any leverage, at the trader's discretion. The LP does the complex part of connecting to the exchanges, managing the risk, and providing the continuous pricing.

Enabling the Ability to Trade with Leverage - or the Ability to Trade Multiple Assets

LPs do not simply provide quotes; LPs effectively enable a leveraged trading model that appeals to retail traders. If a trader opens a leveraged position (for example 1:10) on EUR/USD, essentially the LP is extending credit (through the broker) to provide the trader with a greater, higher yuan based position size, than what the trader could otherwise afford with their capital.

This extends across asset classes. For example:

-

Forex: traders can trade 50+ currency pairs (e.g. EUR/USD, GBP/JPY) with instant execution.

-

Indices: traders can trade, for example, the FTSE, NASDAQ, Nikkei without having to do an actual futures contract.

-

Commodities: traders can access Gold, Oil, Natural Gas using fractional position sizes.

-

Cryptocurrencies: traders can trade Bitcoin, Ethereum volatility without having to own the asset.

Each of these asset classes require either specialized LPs with deeper financial market knowledge and risk management capabilities. If a broker is providing the above instruments, that broker is clearly working with at least multiple LPs behind the scenes, providing liquidity specific to their specialty asset class.

Global Adoption and Regional Variations

The rise of CFD trading across the world has been exceptional, largely due to the fact that institutional liquidity provider (LP) infrastructure has improved execution and lowered costs. Each region presents different adoption characteristics:

Europe: Heavily regulated under ESMA regulation that limits leverage (e.g. 1:30 for major currency pairs and lower for other assets) and negative balance protection. LPs in Europe must have high levels of capitalization and clear reporting.

Australia: Due to ASIC regulation and a strong Web trading ecosystem, Australia has developed into a center for CFD trading. Market and consumer protections assure that LPs have the appropriate risk management structures and brokers trade on fair execution terms.

Latin America: While adoption is in its early stage, adoption of CFDs is growing geographically. Improved access to payer platforms that deliver trading over the internet as well as market volatility of local currencies as a result of inflation has transformed a local Fiat market into a global market. Traders can access the global market while using a USD-denominated CFD account.

Middle East: The Middle East has also witnessed increased interest in CFD trading, specifically on Forex and Gold products. Heads of brokers have express strong intent to set up operations in the region, including partnerships with LPs who can fulfil local demand.

Asia: In Asia, the growth of retail trading conservatively is in the billions; specifically for MetaTrader trading on currency or indices. LPs have expanded their infrastructure considering trading according to the local times, languages and payment methods of the region.

Effects of Regulation on LP Structure

Regulation has a direct impact on the way LPs operate in different jurisdictions. In Europe, in 2018 ESMA implemented product intervention measures that restricted leverage and mandated negative balance protection. Those rules forced LPs and brokers to reevaluate their risk models and pricing structures.

As an illustration, prior to the ESMA rules, European traders were able to trade Forex at leverage ratios of 1:500. After those rules came into effect, that leverage dropped to 1:30 for major pairs, meaning LPs had to rethink their product offerings in order to comply with regulation and still maintain the same level of profitability for lower volume per trade.

In Australia, the ASICs previous focus on execution quality requires brokers to regularly publish slippage statistics and demonstrate that their LPs provide pricing that is fair for their clients. This means an additional layer of accountability for brokers and LPs in order to provide some transparency to traders.

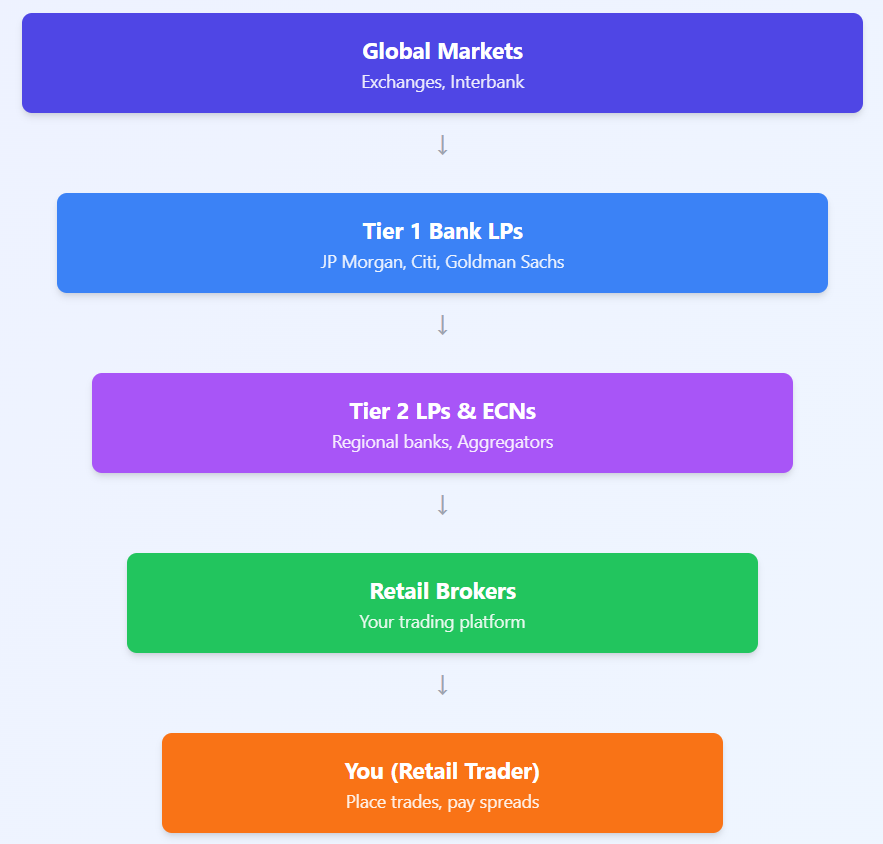

Market Depth Flowchart:

The liquidity flow looks like this, starting from and ancillaries of global markets (exchanges, interbank) → to tier 1 bank lp's that either price in the aggregate, or manage your risk - in either case those LPs must add an additional layer of spread → Tier 2 LPs and ECNs who add more liquidity, or price specialized or esoteric asset classes → Retail brokers who provide the trading platform, and client interface → You who place the trades.

Each layer along this continuum takes a small cut, while providing incremental value. The net effect of the efficiency of the chain from liquidity to retail will shape your ultimate execution quality and average cost of registering your desired position.

Why Global LP Networks Matter for You

When your broker uses terms such as "global liquidity access" or "multiple Tier 1 bank relationships," they are providing you with an assurance that they have invested in a structure to access these LP networks worldwide. This really matters because:

Time zone coverage: An Asian LP will provide better pricing for trades when the Tokyo market is open while European LPs do better when the London market is open. Multi-LP brokers have the capacity to provide execution quality during all hours of trading, 24/5.

Redundancy: If one LP's systems go down or they back-off during volatility, other LPs are there to fill the void. With this redundancy, outages or huge widening spreads are prevented. No LP is bulletproof.

Pricing and competition: LPs have competing relationships for the flow of orders from the broker of their choice. As a result, LPs will provide competitive spreads to the broker, who then needs to pass those savings on to its clients in order to stay competitive in the industry.

The infrastructure of global LPs allowed CFD trading to become available and viable for millions of retail traders around the world. What used to take an institutional connection and millions in additional capital can now be done for a few hundred dollars and an Internet connection. That is the true power of liquidity infrastructure in the modern era.

Key Takeaways: What Liquidity Providers Mean for Your Trading

CFD trading relies on Liquidity Providers (LPs) for its execution. They are part of the foundation behind every trade deciding if it executes instantly or sits in limbo, determining whether you pay 0.8 pips or 3 pips in cost per trade, and establishing if you experience slippage or not.

Here is what is most important to know:

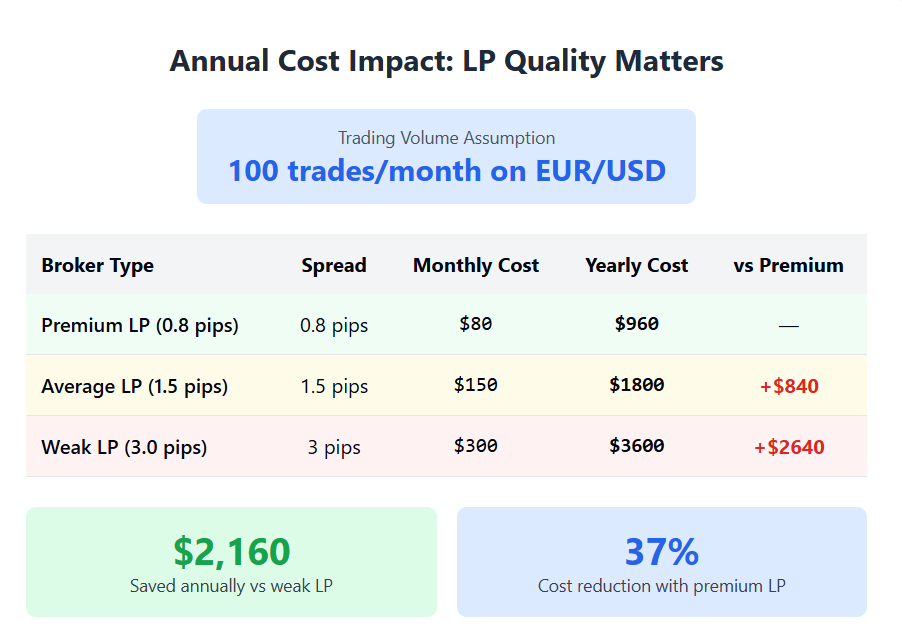

LP directly correlates with your cost of conducting trades; Brokers with connections to Tier 1 banks and ECN aggregators provide tighter spreads which add up over hundreds of trades. That 0.5 pip difference in EUR/USD spreads may in fact save an active trader thousands of dollars each year.

Execution speed indicates the LP infrastructure; When markets are moving quick, milliseconds matter. Brokers with quality LP partnerships will provide execution under 50ms, which minimizes slippage and prevents what you see from not being what you get.

Transparency leads to trust; Brokers that signify partnerships with their LPs, share execution statistics, or operate their business in an ECN-style model are brokers you should consider. They display confidence in their LP partnerships, and provide reassurance that they don’t have hidden markups or platform manipulation.

Trading style will determine what LP you need; If you are a scalper, you need the liquidity of a Tier 1 bank with tight spreads. If you are a swing trader, you can work with LPs in more depth. Trading exotics or cryptocurrency CFDs, you will need an LP with experience.

Importance of regulation: The LP licensing and broker oversight will ensure you receive fair treatment as a trader. Trading with a regulated entity in the UK, Australia, or Europe allows you to complain and ensures minimum operational standards, ultimately protecting you.

Knowing what a Liquidity Provider is, and understanding that it is a provider you should evaluate a broker through is an eye-opening evolution in your mindset. Instead of focusing on and comparing spreads publicly available on a marketing page, you will start to ask deeper inquiries:

Which LPs do you trade with? When you trade with an LP and experience volatility, how do you manage execution? Can I see real-time depth of market? Asking these types of questions opens up insight into the infrastructure holding your trade.

What now? If all of this is new and exciting, then experience it.

Open a demo account with btcdana and test out the LP execution environment. Experience different instruments during volatile periods. Fill a few different trades at various times of the day, then compare those fills, this is a great way to reinforce (or separate fact from fiction!) the quality of liquidity. You will learn more about the quality of liquidity by doing this than you could ever learn from reading an article.

Successful traders do not only consider fees; they know how their liquidity is being serviced. This is what separates successful long-term trading from being frustrated with quality execution and hidden costs.